These are the three macro forces we will invest behind in the decade ahead. The value of human labor is being undercut by synthetic intelligence. The hegemon which built the current world order is actively undermining it. The pace of reproduction and the arc of a human lifespan are evolving.

These megatrends overlap and reinforce one another. Dropping birth rates and aging populations provide a natural incentive for greater automation. Automation increases self-sufficiency, reducing the need for incremental interconnectedness in a multi-polar world. Fewer young men points to more automated warfare. Near term, the investments in automation, in self-sufficiency, in rearmament, in rising healthcare costs point towards unsustainable government finances which will only be saved by more aggressive productivity boosts, brought on by automation...

While the quarterly fluctuations will be material, these are structural forces unlikely to slow. On a ten year time horizon, it is better to be positioned with them as persistent tailwinds.

Incrementally, as capital replaces labor, having the correct model of the world and investing with conviction behind it becomes the primary avenue of wealth preservation and enhancement. Previously, wealth helped one to enjoy the limited time allotted. In the decades to come, it may be swapped for time itself.

We are less than four years into the largest technological revolution the world has ever seen. We will shortly be joined by billions of new economic actors in the form of agents, followed by their embodied counterparts. The acceleration in production, in scientific discovery, in workplace disruption will be unprecedented.

This wave is coming at a time where existing institutions are stretched to the brink: >85% of US voters are frustrated with the opposing party. Debt to GDP globally is >300%. Global supply chains are now a bug, not a feature. Domestic inequality is elevated. Fiat currencies are a fifty year old experiment. The US is pulling back from its role as global hegemon.

And yet, as investors, as young people, as parents, we have never been more optimistic. The Economic Possibilities for Our Grandchildren have perhaps never been more promising. Instead of B2B SaaS and consumer internet marketplaces, the entrepreneurs of the 2020s dream of data centers in space, interplanetary travel, abundant clean energy, aging reversal, and machine gods.

History is on the move once again. Ambitions are moving in lock-step. Our industrial-era institutions are shaking while the machine age is struggling to be born.

It's impossible to say what the world will look like in 2035, but it promises to be much weirder. Much more unpredictable. Much more amazing.

All at once.

1. AI and Automation

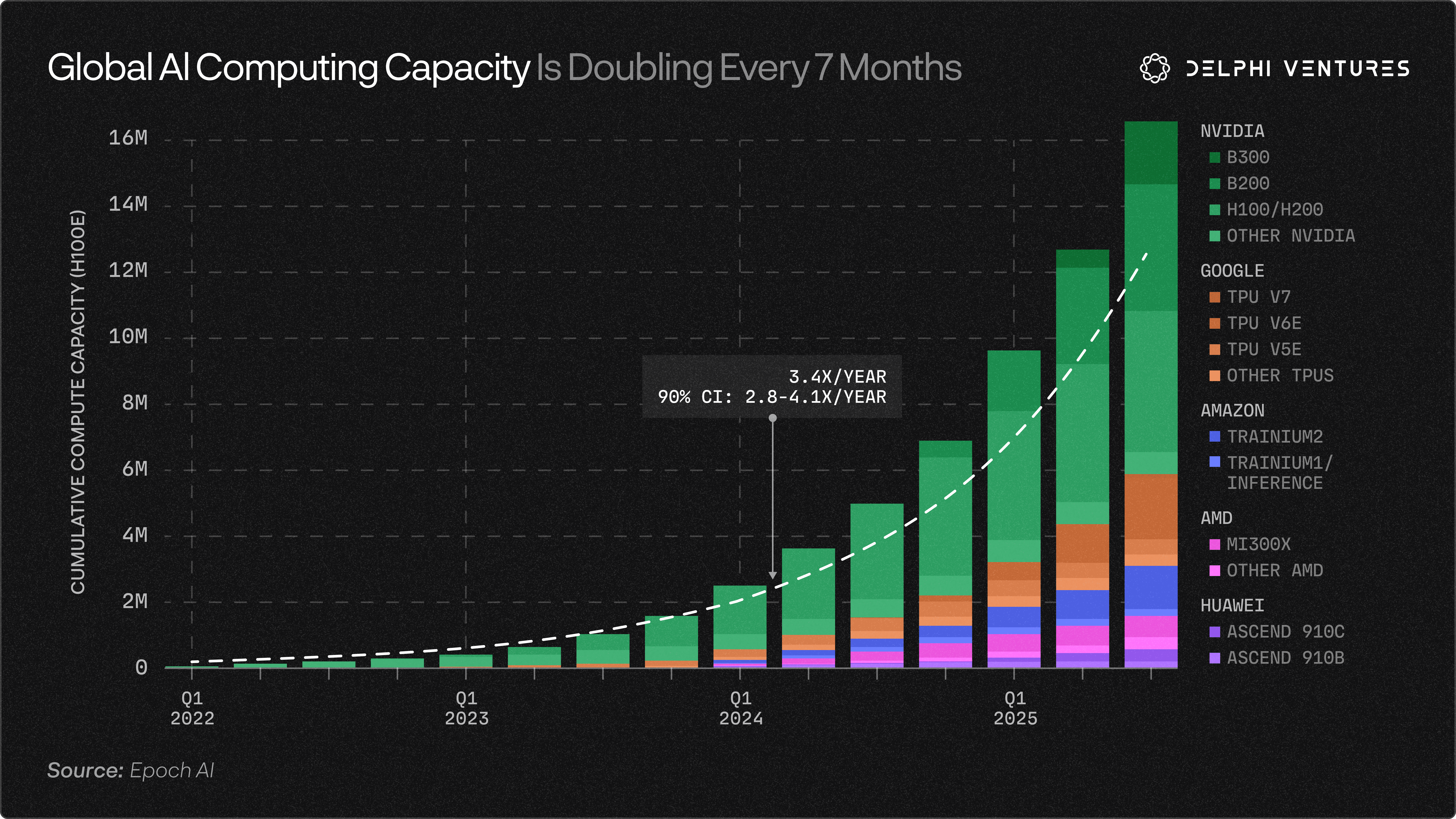

In three words, “Leopold was right.” At basically every juncture, the entrepreneurs, investors, and pundits betting “we don’t have enough compute” have stayed winning. Again and again and again.

The Palo Alto to New York arbitrage remains intact.

We can now turn silicon and energy into intelligence. Bottlenecks emerge — compute, data, power — and are struck down, increasingly with the aid of the synthetic counterparts now being cultivated.

The capabilities continue to accelerate...

While the flops continue to grow…

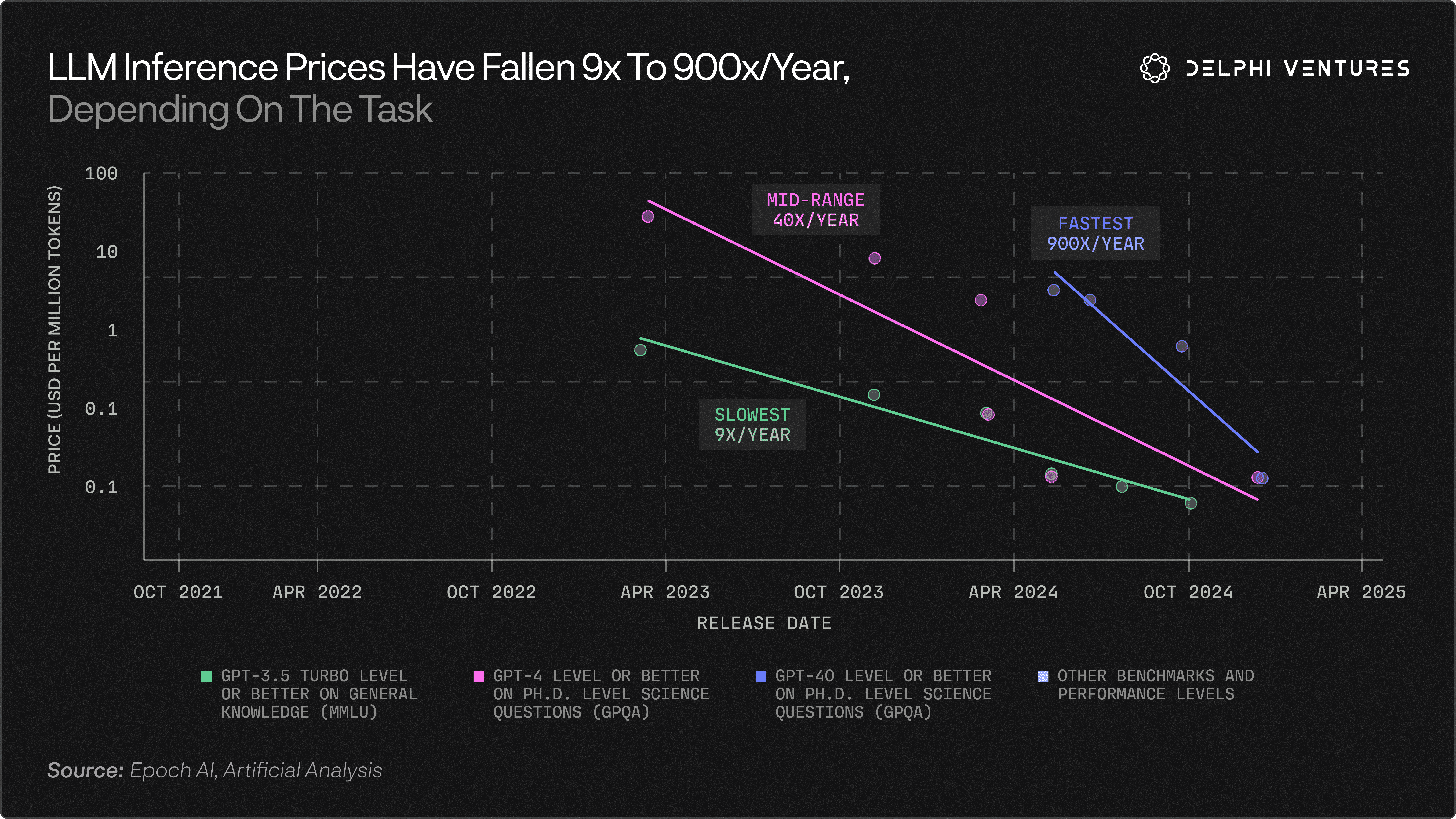

While inference costs continue to plummet...

While the traction is inflecting..

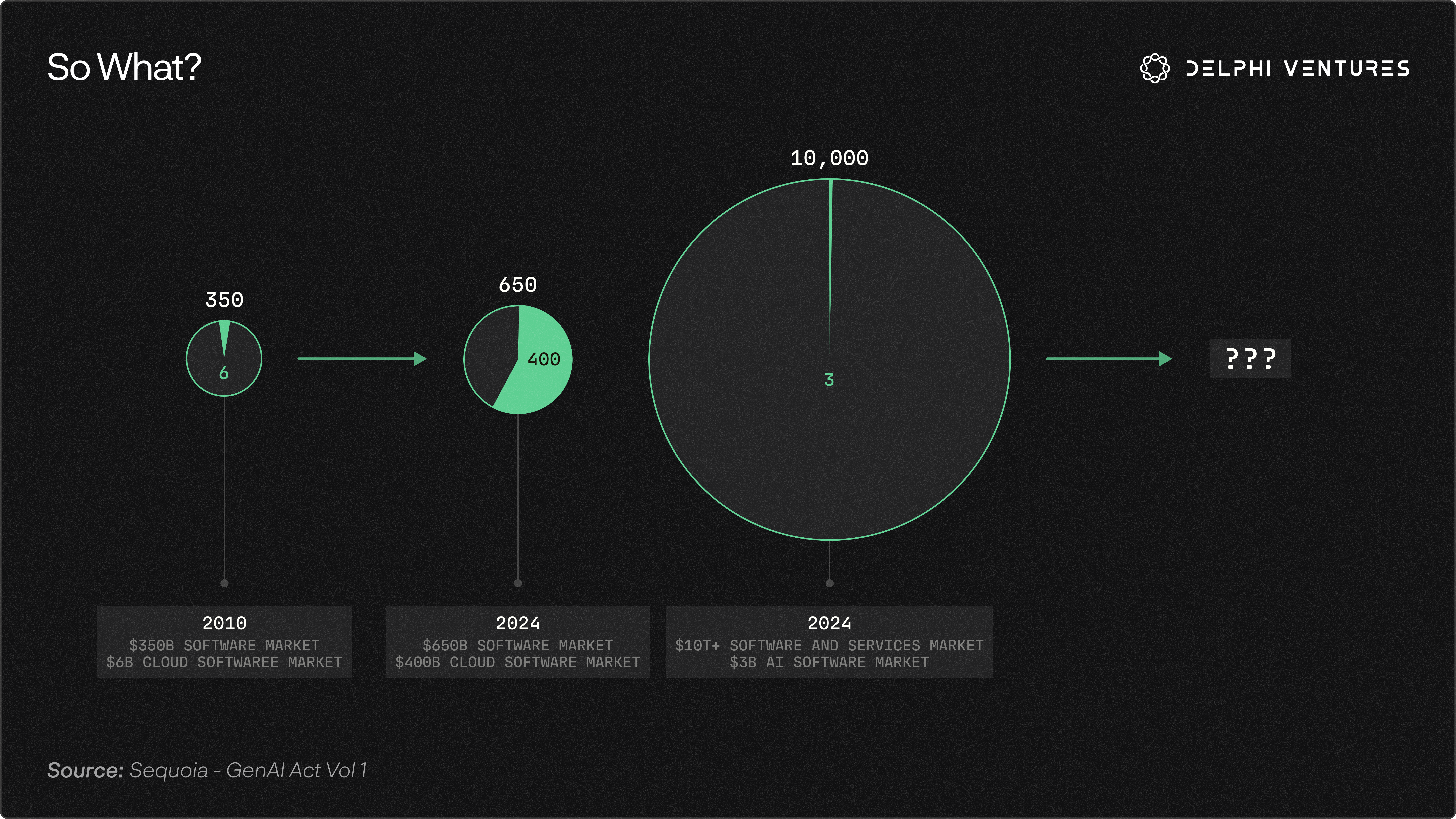

Targeting a TAM of a significant portion of all white collar services globally...

Likely expanding to physical labor as well... (probably much too conservative)…

Perhaps a concise way of saying this is: “the demand for intelligence appears uncapped.”

And here is the part the bears never priced correctly: efficiency was supposed to kill the trade. DeepSeek was supposed to be the moment the music stopped. Instead, every collapse in the cost of tokens doesn’t shrink the market, it floods it. Each order of magnitude down in price drags a thousand workloads above the waterline that were previously uneconomic. We do not have a compute glut. We have a demand function that wakes up hungrier every time we feed it.

The relative winners may shift, but the pull remains constant.

Getting Religion

Increasingly, investment under- and out-performance depends on how early - relatively speaking - allocators became truly “AGI-pilled.”

There is a small circle whose epicenter arose in San Francisco in 2022 but has been rippling out (surprisingly slowly) over time. Neurodivergents in Hayes Valley, lurkers in Less Wrong forums, OpenClaw hosts in Liangzhu, and increasingly, the board rooms of the world’s largest companies, who “got religion” first. The rewards have been handsome.

Skeptics are increasingly being brought to heel.

Increasingly, industry after industry will be held up before the machine god to be judged worthy or unworthy. To become fuel for model acceleration or prepare to be devoured.

However, the machine god’s appetite is constantly evolving, needing more and different inputs to feed its growing ambitions. LLMs milked decades of internet text. Diffusion models, the photos. Video models were the obvious next step. Truly agentic workflows are piecing them all together and more, requiring live multimodal environments on which they can be RL’d to perfection to deliver longer and longer time horizon tasks.

Still, this first era of largely digital AI feels trapped. Overly wedded to language. Overly digital. Chained in the data centers.

The next phase of AI promises to deliver more holistically on the original promise of the internet of things. An internet of intelligence. Interactive networks of ambient, distributed AI, mixing cloud and edge, the digital and the physical, reasoning and latency, performance and cost. Learning continuously.

The next phase of AI looks something much closer to Jarvis, but at global scale. Injecting AI capabilities not only into white collar workflows but into the entire value chain of production.

The silicon towers of Babel will continue their heretical ascent towards the heavens, but they will be complemented by much lighter, more nimble, and interactive distributed networks which are reciprocal in data → model performance feedback loops. Ambient computing and continuous learning will emerge as flavors du jour.

2035 looks much less agentic RL and much more Elon-pilled: SpaceX x xAI x Tesla x Optimus x Neuralink x Starlink all coordinating and complementing each other, ideally across much broader swaths of the economy in modular networks.

Guiding Investment Themes

- The Agentic Economy is imminent. The internet is rapidly being remade for agents.

- Indexing, discovery, payments, commerce will all be rapidly redesigned for an economy in which agents become the primary consumers and producers of digital information.

- Networks which most efficiently orchestrate data, compute, and intelligence will be immensely valuable - from vertically integrated companies to fully distributed networks and hybrid stacks in between.

- The demand for intelligence will continue to outpace supply for the foreseeable future.

- TSMC fabrication capacity remains a bottleneck on bullish euphoria, capping supply where the worst excesses of the fiber-optic overcapacity seem unlikely.

- Assume scaling laws remain intact until proven otherwise. The more compute = more capabilities, which = more demand for compute has proven potent. Invest behind the centralized performance bottlenecks: memory, power, EUV, fab capacity, Photonics, space-based networking, etc.

- The best people now have significantly more leverage.

- Power-laws in capital, talent, and value capture / creation will only increase, and the price paid for the few individuals who can marshal them effectively will go up significantly.

- Barbell: the best times to invest are a founder and an idea, or a US$100bn company on its way to multiple trillion, playing the biggest upside or the most probabilistic compounding.

- APIs to the real world are the next logical frontier.

- Language is insufficient for properly understanding and acting in a complex world. The trillions in capex on data center spend will increasingly be diverted towards helping digitally native intelligence understand and have agency in the world of atoms.

- The next phase of AI will tilt towards the edge: hybrid edge-cloud networks which recognize the material trade-offs between cost, latency, and privacy necessary for AI to escape the data center.

- 3D Printing

- Novel materials

- Precision manufacturing

- Reduce extended supply chain dependencies in specialized categories

- Macro implications.

- Capital is scarce again: rates stay elevated near term

- Polarization continues: K-shaped economy exacerbates as the majority are one-shotted by cheap dopamine while a few transcend.

- Caution regarding assets leveraged to consumer spending built on services labor (mortgages, credit, consumer, etc).

- Sharp pivot left in politics as inequality spikes and anti-AI sentiment rises, leading to higher taxes, more surveillance, and greater capital controls.

- Initial inflationary spike in inputs, followed by massive deflation in services and then goods.

- “Catchup growth” from globalization reverses - AI winners start pulling away; China may be the last emerging economy to climb the manufacturing-led path to relative prosperity.

Potential Seed Sweet Spots

The macro is fairly consensus; the entry points are not. Hunt for compounding edges the model can’t swallow:

- Vertical Data Foundries: As inference races to zero, the scarce input becomes verification - the data and RL environments where truth is expensive to establish. Look for categories where reality is hard to label (bio, robotics, hardware/EDA, law, materials).

- Agentic compliance: Everyone is shipping “agents.” The core challenge is consequential, legal, insured action - moving money, prescribe, file, dispatch, sign - enabled by some sort of license, bond, or the insurance.

- The grid revamp: Behind-the-meter power, interruptible training-as-load, data-center thermal, and the fragmented, dual-use long tail of reshoring: advanced packaging, chiplet interconnect, specialty materials, etc.

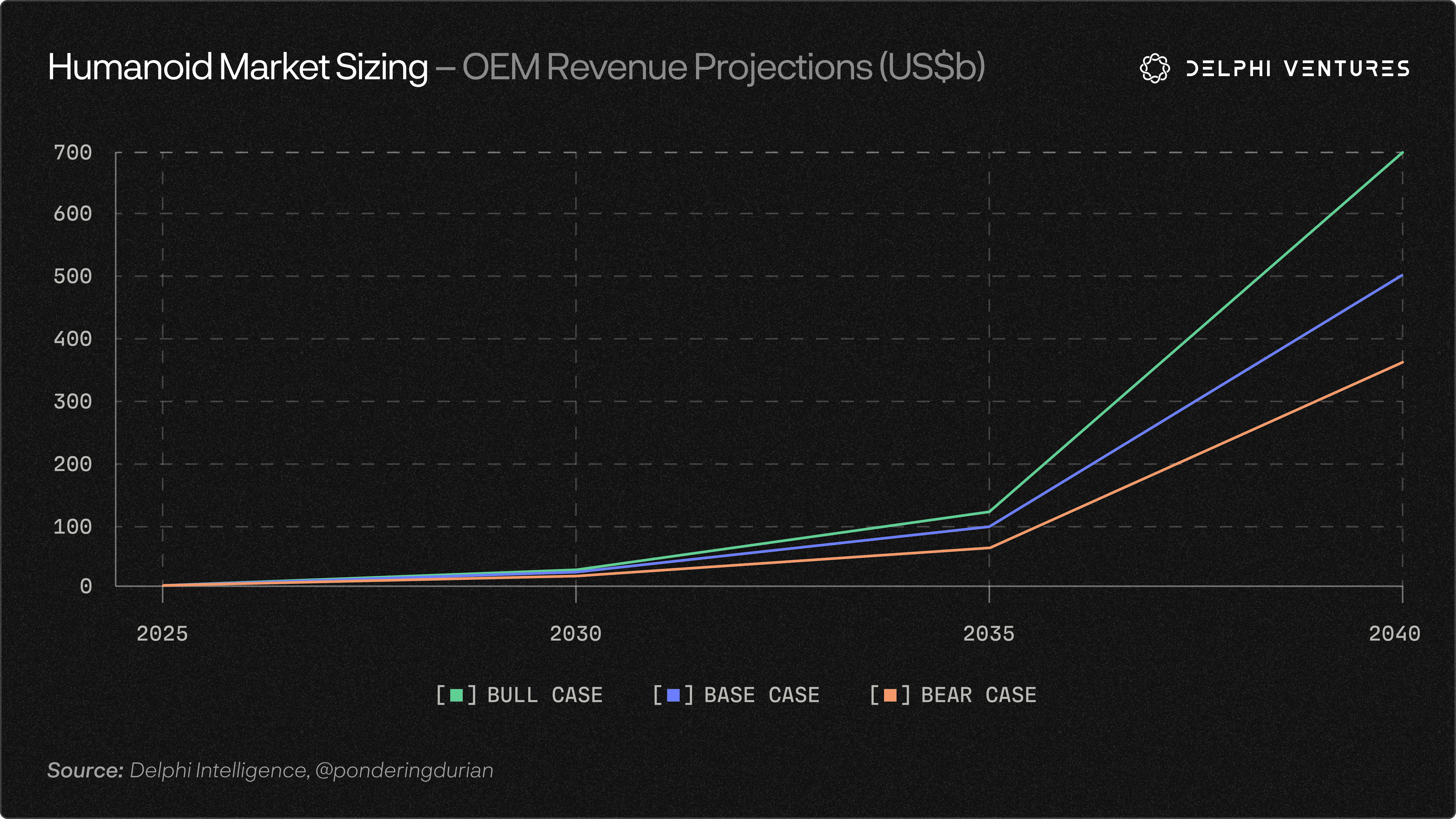

- Data flywheel for Embodied AI. Bet on leaders that ship real volumes early and in-house core components - the flywheels will compound quickly in what is one of the largest TAMs in history.

In short, prepare for a world in which we do not have a compute glut but remain intelligence-constrained. A world in which software becomes abundant. A world in which agents, not humans, become the primary economic actors. A world in which AI infiltrates the physical world via hybrid networks. A world in which scientific discovery accelerates, diseases are cured, GDP growth flirts with double digits, we retake space - and yet, political unrest spikes, demographics reach crisis levels, asset seizures and nationalization become normalized, and measured IQ slide downward....

In any given quarter, expectations may get ahead of reality. On a ten year horizon, the world has fundamentally shifted and too few have yet to recognize the full implications.

In short, what if it’s not a bubble?

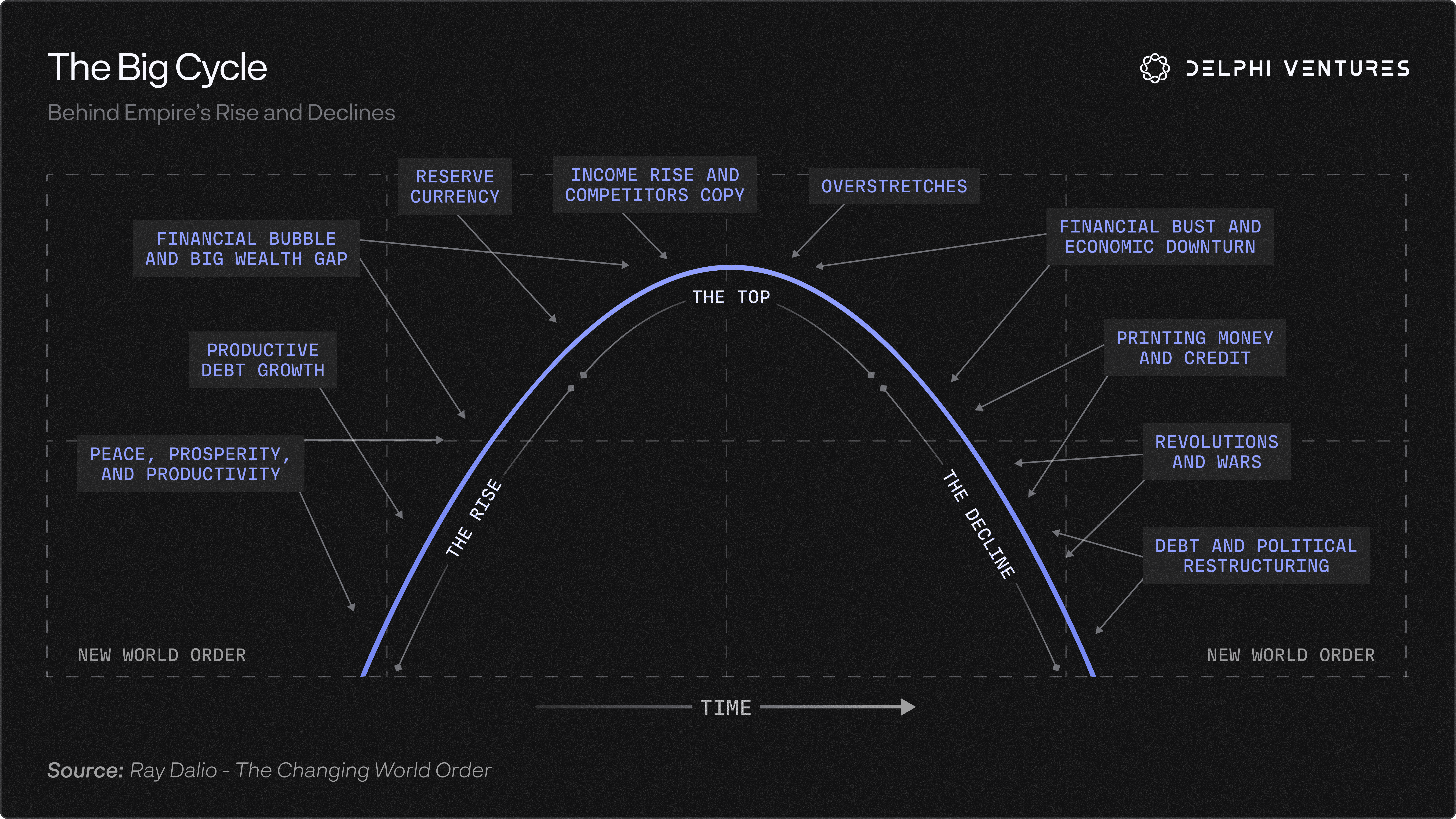

2. Multi-polarity

The second election of Donald Trump in 2024 was a referendum by the American people on the existing world order. An order first emerging in 1945 and entering hyperdrive in 1989 with a triumphant American liberalism remaking the world in its image. Global supply chains, free capital flows, a shrine built to a singular, all-powerful deity: the American consumer.

It has now been rejected.

The peace dividend and material abundance brought post-Bretton Woods has been undeniable, yet its very structure held the seeds of its ultimate demise. The inevitable tensions of liberalism and national interest. Of meritocracy and inequality. Of global capital and domestic labor. The Triffin dilemma proving inescapable: a democratic society enjoying reserve currency status hollowing out domestic industrial production in exchange for paper IOUs, waking up decades later to find a near-peer rival with a different view of societal flourishing underpinning production of the material goods to which it has become addicted. The supply chains which underpin its multinational corporations. The factories which fuel its military might. The lenders which enable its fiscal deficits.

The twin pillars of national security vulnerabilities and the relative stagnation of middle America kick-started a countdown on the eighty year old world order.

So... what now?

The hegemon which built the post-Cold-War globalized world order at the end of history is now turning on it. The leader which policed the seas, fostered global supply chains, insured safe passage of energy and goods, ran deficits to fuel the machine’s endless consumption, and opened its capital markets to the world as a safe haven in which to recycle those trade surpluses, is well...

Nation states are now left scrambling to shore up the obvious vulnerabilities emerging in its wake. This renewed focus on redundancy, energy security, technological sovereignty, and military rearmament in a more hostile, multi-polar world is undoubtedly bullish for fiscal deficits, commodities, and the secular inflationistas, all inconveniently occurring at a time of unprecedented global debt.

The obvious investment opportunity then is front-running each pole as it races to shore up its own house amidst the divorce.

But the second order implications may be less obvious.

The End of the World is Just the Beginning

As Peter Zeihan lays out in his book by the above title: globalization is fragile. Globally optimized supply chains, the free flow of energy, the low cost of insurance, the dearth of military conflicts, the ability to tap the lowest cost labor - all combined under an American hegemon to allow for a symbiotic relationship where rich countries could continue to consume disinflationary goods and poorer countries could climb the agriculture → low cost manufacturing → urbanization → services ladder to greater material well being.

This system is being unwound.

Ever since the freezing of Russian assets and the blocking of the Strait of Hormuz, there is no longer a guarantee that US treasuries can be quickly converted into energy. There is no longer a guarantee of American-sponsored security.

As nation states race to shore up dependencies from global supply chains... while they rearm amidst American retrenchment... while they diversify away from US treasuries... while they look to shore up energy reserves... while there is an AI capex supercycle underway... the mispricing of commodities, energy, and hard money on a ten year horizon is clear.

However, the country which enabled such a system - the United States - is also the one best positioned to withdraw from it with minimal consequences. The US is surrounded by friendly neighbors. It has the most powerful military in the world. It is energy independent. It is food independent. It is leading the AI revolution. It will need to cut back on consumption in order to properly reindustrialize, but that is uncomfortable, not catastrophic.

The US pulling back from the existing world order is a bigger problem for everyone else, and almost no one - with the possible exception of China - has been preparing for it. We have seen this with natural gas in Europe after the war in Ukraine. We have seen this with the energy crisis unfolding across East and Southeast Asia in the wake of the closing of the Strait of Hormuz. We have seen this with expat flight from the Middle East amidst an unexpectedly extended conflict.

In a game of modern mercantilism, the US is best positioned to become more autarkic. China is naturally in a significantly worse position - surrounded by hostile powers, energy dependent, food dependent, tech dependent - but that is exactly why it has been investing existentially in renewables, semiconductors, military build-up, and food security. China has been keeping its exchange rate artificially low for decades, reinvesting surpluses into areas of strategic vulnerability in preparation for a multi-polar world.

Other countries have not.

Under the mass industrial paradigm, many developing economies’ biggest asset was abundant, low-cost labor as capital scoured the globe for ever cheaper inputs. In a world where sea lanes are hostile, insurance prices increase, and energy prices remain elevated, capital and compute rich countries will invest in automated production at home. The demographic dividend becomes a demographic liability.

While the 2000s–2020 were decades of globalization, harnessing abundant human labor, and convergence as “developing” economies “caught up” to their “developed” counterparts, the decade ahead promises to reverse these mega trends. Countries with abundant capital, elite frontier technical talent, scale AND the political will to fully implement AI and robotics will reaccelerate. The rest of the globe will likely be carved in two: those blessed with the relevant natural resources or niche industrial processes to serve the AI, robotics, and military supercycles, and those left over with large swaths rapidly depreciating human labor.

The pair trades are pretty clear.

Potential Seed Sweet Spots

The macro screams “long commodities, short bonds” - but those aren’t seed checks. However, the divorce throws off a litter of fundable, founder-shaped problems:

- Reshored processing: Rare-earth separation and magnet-making (China owns ~90%), uranium enrichment and HALEU (Russia-dominant, and every SMR startup’s silent dependency), and the de-DJI-ification of the Western drone stack - motors, flight controllers, optics.

- Tooling for reshorers: Every reshorer now has a “qualify a second supplier” problem. Sub-tier supply-chain mapping, chokepoint-exposure intelligence, friend-shoring sourcing marketplaces, supplier-qualification software. The software stack which assists a vast reshoring effort.

- Open weights are emerging as the default substrate for the non-US world. The serving, middleware, and tooling layer around open models is the obvious stack for the cost-sensitive Global South and for any enterprise allergic to US frontier lock-in.

- Long the repricing of risk itself. As the US stops underwriting the sea lanes, the world’s insurance premium goes up. Parametric and war/political risk insurtech, supply-chain-disruption cover, geopolitical-risk pricing intelligence. Everyone is crowding into neo-defense primes, but the firms repricing this risk stand to benefit materially

- Verticalized Farming & Genetically Edited produce: Dutch model gains traction globally; weather-resistant strains of food crops to combat extreme weather

- The Triffin paradox has a plumbing layer. As official-sector dollar recycling reverses, street-level dollar demand in emerging markets paradoxically rises - de-dollarization at the central bank, dollarization on the corner. Stablecoin dollar-access and trade-finance rails continue to proliferate.

3. Demographics (& Longevity)

In 1950, four countries had birth rates below replacement. In 2024, that number is 136 (71% of the globe). China’s TFR has dropped to ~1.0, suggesting population shrinkage to the low hundreds of millions by 2100. In Italy, Portugal, Greece, Japan and Korea, over one-third of the population will be >65 by 2050. 10k US boomers turn 65 every day and the Social Security trust fund is projected to be insolvent in the early 2030s.

We are living longer and having fewer babies.

The impact on fiscal budgets, elderly care, healthcare costs as a % of GDP, and workforce participation are obvious. The industrial-era welfare state is predicated on maintaining birth rates above replacement; a ponzi fueled by contributions from ever more youthful participants. With the rapid inversion in demographics brought on by modernity, the model is broken.

So... who is going to foot the bill for the outstanding liabilities?

The most obvious, and likely, solution is a combination of debasement and a sprint for automation. A cocktail of money printing, higher taxes, agentic productivity, and robots.

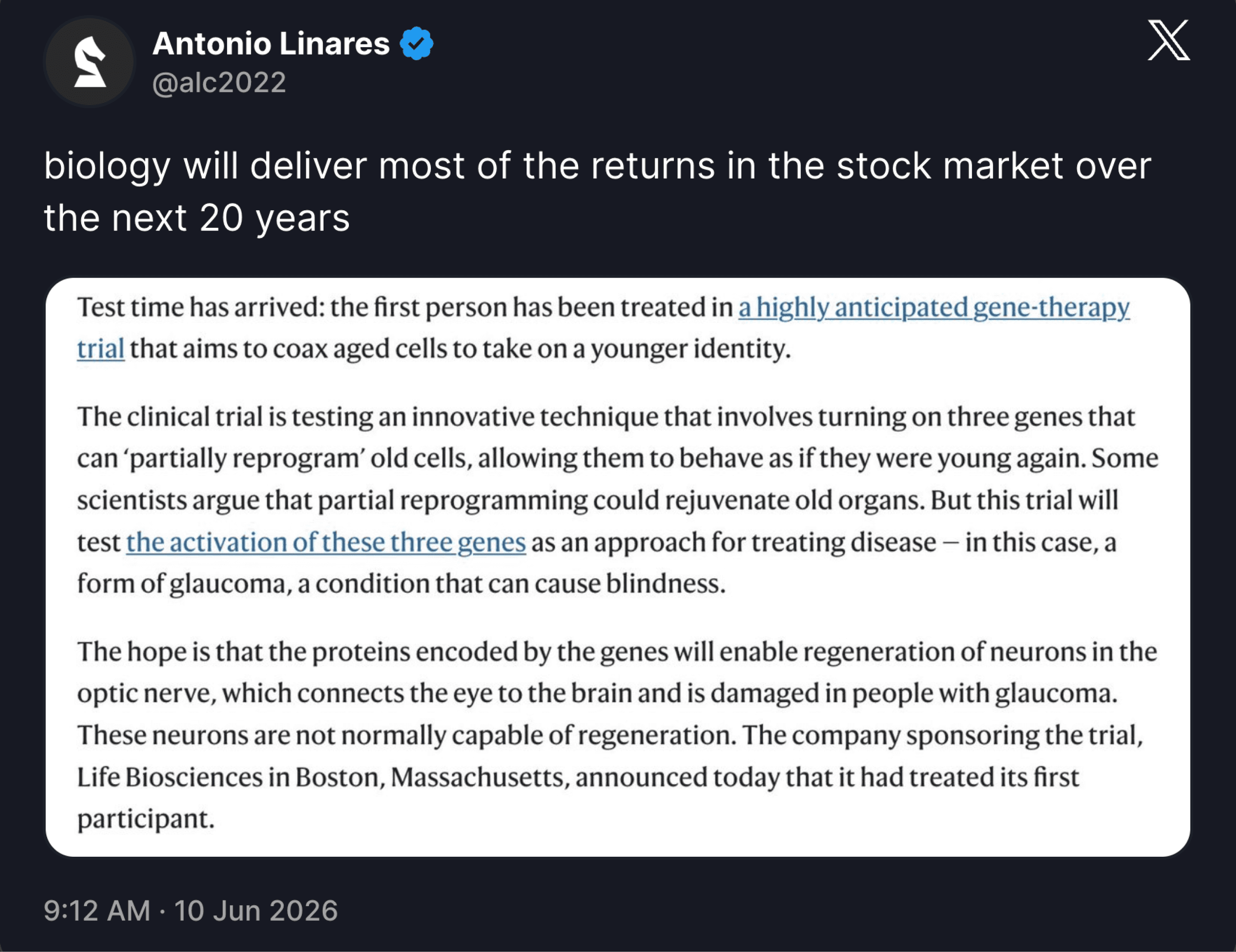

However, another, more optimistic case is showing green shoots. Expanding human lifespan to enable more, healthy years of productivity. Yamanaka factors show clear signs that cellular aging reversal is possible. Longevity-focused companies from NewLimit to Altos Labs to Life Biosciences are receiving billions in funding. Each is going after specific organ diseases given the structure of the FDA, but the grand ambition is to treat aging itself.

As opposed to the massive capital investment and spiking valuations across AI and robotics, market enthusiasm at the intersection of AI x Bio has remained surprisingly muted until very recently. The sector’s come-down from the 2021 highs was particularly brutal, but the ungodly compute coming online is providing novel insights into previously locked molecular mysteries - protein folding, polygenic traits, cellular mechanisms - increasingly wrestled into the realm of the legible.

To paraphrase Demis Hassabis: “if math is the language of physics, then machine learning is the language of biology.”

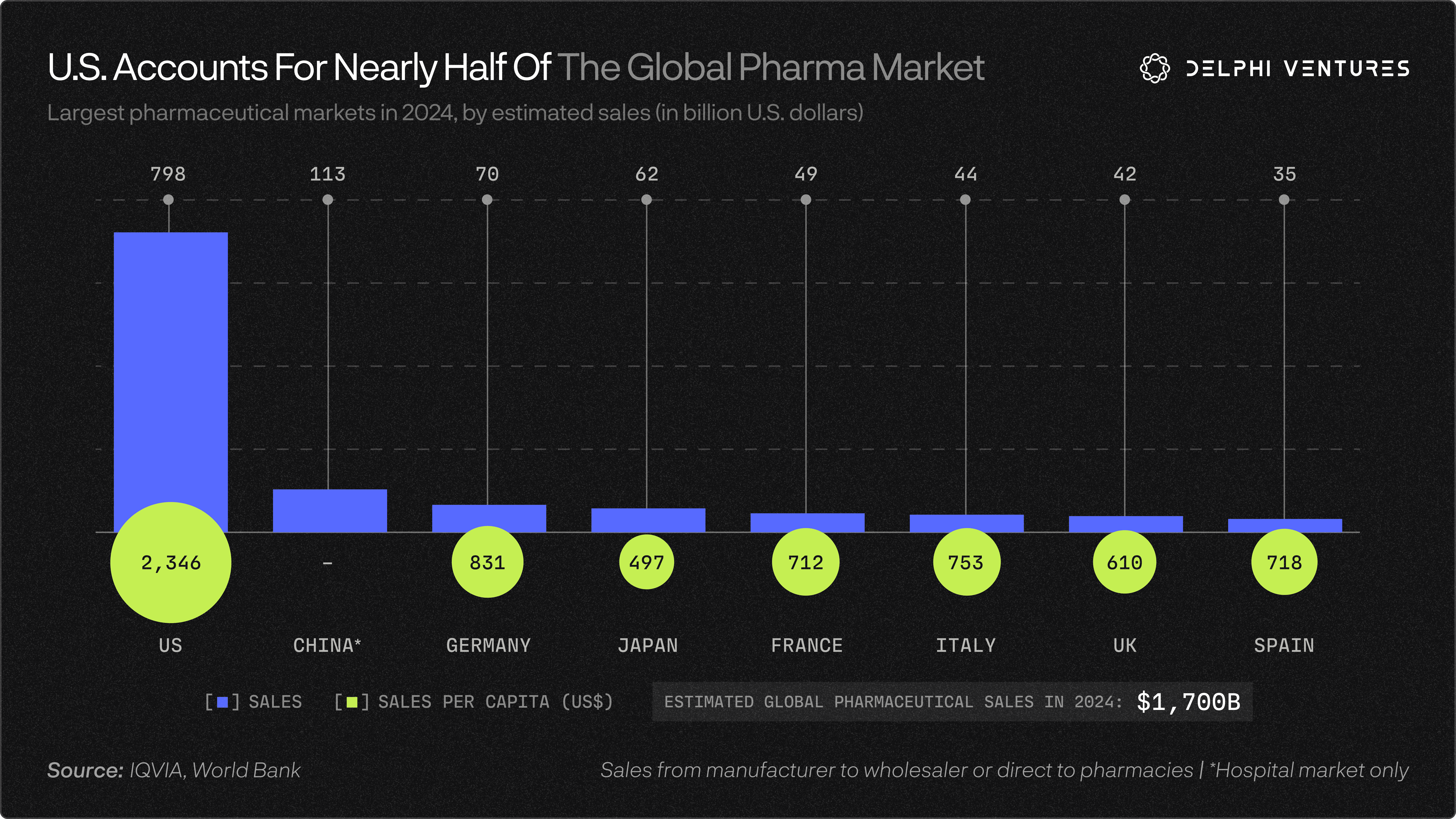

This is a large pie.

As our understanding of biological mechanisms becomes more precise, it’s hard not to see these figures rising significantly. GLP-1’s are just the tip of the iceberg.

Once you can edit genomes and reverse aging in cells, it seems likely the majority of post-scarcity disposable income would slide in this direction. In the grand scheme of economics, the only real currency is time. By training our millions of GPUs on life’s most atomic units, the 21st century’s greatest achievement may just be that we learn how to manufacture more.

In the medium term, my hope is that AI’s greatest gift to humanity is expanded lifespan, which would boost later-life productivity significantly, helping us tread water demographically until the humanoids are deployed at scale.

In the long run, my hope is that the deflation brought on by AI will lead to a recovery in fertility. Embryo screening. Fertility advances. Synthetic wombs. Cost reductions in childrearing. A 50% reduction in the number of hours worked. I suspect the 21st century will see a material shift from crafting identity around work to crafting identity around individual passions and family.

We hope our investments can play a small part in pulling this future forward.

Potential Investment Areas at Seed

- Longevity is data-starved: Aging clocks need longitudinal multi-omics data which is scarce. Biomarker and biological-age companies, at-home multi-omics sampling, and eventually implantable biosensors, the consumer wedge that quietly mints the training set.

- Human augmentation: enhancement/accessibility of vision, speech, mobility etc

- Brain Computer Interfaces: human-AI interfaces bypassing skin and language barriers for tighter feedback and faster bandwidth communication

- AI for the trades: Reshoring + the grid buildout + demographic collapse all converge on a shortage of electricians, plumbers, HVAC techs, and linemen.

- The fertility frontier: Synthetic wombs are still early, but in-vitro gametogenesis, IVF automation, and polygenic embryo screening all present real opportunities.

- The demographic dividend: the 60–80 cohort is the richest underserved consumer market in history. Decumulation fintech, longevity-risk products late-life productivity tools seem like underexplored categories

The Tug of War: The Paradox of Technological Acceleration

So, it seems we are caught in a catch-22. Without technological acceleration, we will be stuck in a demographics, deficits, degrowth doom loop. With technological acceleration, we risk more elevated p(doom) scenarios and runaway inequality fueling further polarization.

Our view is that technological acceleration is the only real option; one which will require prudent management and proactive efforts to diffuse benefits to ensure societal support.

Debt / GDP is already >300%. The demographic pyramid is inverted. Fiscal deficits are elevated and only projected to increase. Across almost every vector, massive investments are needed in reindustrialization, national security, climate transformation, grid capacity and more.

As Ray Dalio reminds us, in every debt crisis where debts are denominated in a local currency, governments inevitably print. Stuck between austerity, mounting debts, and rising yields... the inevitable outlet is the currency.

To quote Keynes quoting Lenin: “There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency.”

These discontents are erupting in real time.

Populist politics is on the rise globally. Rising living costs are a major culprit. Money creation is outpacing production. Deficits - when looking at the reversal in globalization, the costs of rearmament in a multi-polar world, the rising costs of healthcare in aging societies - are only set to increase.

Paradoxically, automation is the only real outlet available to stall the fiscal doom loops in which most nation states have found themselves, and yet the structural inequality it delivers will almost certainly receive the backlash which will make it difficult to implement. The biggest barriers now are political.

The obvious question becomes: what pace of acceleration will society tolerate and how do we make sure the gains are more broadly distributed? Increasingly, given the centralized nature of value creation to massive corporate entities, it seems unlikely that purely market forces will lead to a politically tolerable outcome.

To me, four futures unfold before the West which are dynamic and reciprocal in nature:

- Techno-feudalism: Continue on our current trajectory without adjustments: capital is rapidly converted into agentic and embodied intelligence with massive gains held by narrow pockets in SF and New York. Owning small slices in the compute and data flywheels is the answer, but likely to lead to political resistance like...

- Chinamaxxing: political discontents lean towards a authoritarian, repressive state enabled by advanced technology: greater capital controls, higher taxes, more surveillance in exchange for greater safety, convenience, stability, and public works. However, this overcorrection would create a backlash from the makers in a world where capital and talent are mobile, fueling the...

- Flight to the network: Balaji’s libertarian unraveling of the industrial-era institutions: capital flight for friendlier jurisdictions, crypto wallets, distributed AI, and fiscal strain on those left behind. Or...

- We muddle through. We find our way through the narrow corridor, accelerating enough to avoid the doom loop with enough diffusion / redistribution to keep broader society onboard - leading to a golden age within the existing institutional framework, not a complete overhaul.

Before the intelligence boom, scenarios two and three seemed surprisingly high probabilities. The Delphi Ventures thesis was therefore heavily wedded to crypto: building a better, uncorrupted parallel system of exchange, collaboration, and wealth preservation while the structural realities of demographic inversion, rising deficits, political division, and debasement took their toll.

The barbell approach between hard assets and alternative internet-based stores of value is still a compelling way to hedge these megatrends: front-running nations as they shore up dependencies - longing commodities, energy, and defense against fiat and bonds. Front-running debasement and confiscation in Bitcoin, Zcash, and the distributed agentic economy against non-G2 emerging markets and bankrupt municipalities.

However, with the intelligence revolution emerging in November 2022, it increasingly seems likely we just might have found a golden ticket: a productivity boom over the next ten years which can overpower the overhang brought on by demographics, deficits, and debasement.

Previously, we were backing entrepreneurs building outside of existing institutions. We will continue to do this. However, given this evolution, we will also invest in the very best people within the existing paradigm, because it is being reborn before our eyes.

Yes, the challenges are daunting. We are staring at massive debt loads, spiraling deficits, political polarization, cost of living crises the world over, the return of war and great power politics, and rogue AI risks. Watching the news or X feed, it’s hard to feel like it’s not hopeless.

Don’t fall for it.

By 2035, the world and near orbit will be awash in accelerated compute. We are seeing inflections in agentic capabilities, robotics, rocket launches, advanced materials, novel therapeutics, and more.

The future belongs to the optimists. Invest accordingly.

We certainly are.

Thanks to @ZeMariaMacedo for initial idea for this article, @cannngurel for the feedback, and Neco from @Delphi_Design for the graphics.

@PonderingDurian, signing off

.png)