Introduction

This report is for overseas investors exploring AI investment opportunities in China. It provides a market primer—helping you build foundational knowledge of China's VC ecosystem, active investment players, and AI sub-sectors before your China Trip.

A caveat: this is not a comprehensive investment guide. It does not cover risk analysis, exit environment, or legal structuring. These topics are equally important but fall outside the scope of this document.

Disclaimer:

GPs and companies mentioned herein are for informational purposes only and do not constitute investment advice or recommendations.

Part 1: China VC Market Overview

1. Market Players

China is the world's second-largest VC market, but its ecosystem structure differs fundamentally from the U.S. Understanding "who's deploying capital and with what kind of capital" is the first step to understanding China's innovation ecosystem.

1.1 USD Funds

Representative firms: HongShan (formerly Sequoia China), IDG Capital

USD funds were once the dominant force in China's VC market—nearly every mega unicorn from Alibaba to ByteDance had USD fund backing. However, geopolitical pressures and reduced LP commitments to China over the past few years have put USD GPs through a painful contraction period. In 2023–2024, several top-tier USD GPs completed brand separation and rebranding due to geopolitical factors (e.g., Sequoia China became independent as HongShan). Meanwhile, most USD funds became extremely cautious, with some effectively in hibernation mode.

But entering Q1 2025, sentiment reversed dramatically. Following the release of DeepSeek R1 and Manus, USD funds collectively entered a FOMO state, deploying capital at a rapid pace. Details in Part 2.

1.2 Market-Oriented RMB Funds

Representative firms: Shenzhen Capital Group, Fortune Capital, CICC Capital

RMB funds are currently the most active investment force in China's primary market. This shift occurred over the past three years. As USD funds pulled back, RMB funds filled the vacuum. By deal count, RMB funds account for over 80% of market transactions.

The largest LP source for RMB funds is Government Guidance Funds (national-level to provincial, municipal-level).

RMB fund investment strategy is not always return-driven. Government LPs sometimes attach reinvestment requirements (mandating that a certain percentage of fund capital be invested in local enterprises) and industrial policy mandates. Preferred sectors for RMB funds include: semiconductors/chips, advanced manufacturing, embodied AI, foundation models, and new energy.

1.3 State-backed GPs & Funds

Representative examples: Beijing and Shanghai's RMB 10bn+ AI industry guidance funds

Some governments have evolved from "capital-contributing LPs" to "direct investors." Common operating model: Local governments partner with established VCs to set up dedicated funds, with VCs handling investment management while government-affiliated investment vehicles serve as co-GPs.

1.4 PE Funds Launching Early-Stage VC Funds

Representative firm: Primavera Capital

China's PE funds, whether USD or RMB-denominated, are not particularly active in the current market. This is because PE funds' traditionally preferred sectors (consumer, retail, services) are not seeing active deal flow. Some PE firms are attempting to pivot: extending into early and growth-stage tech investing.

1.5 Corporate Venture Capital (CVC)

Representative firms: Alibaba, Ant Group, Tencent, ByteDance, Xiaohongshu (RED), Baidu.

CVC investment styles vary significantly across firms.

1.6 Super Angels

Successful founders and internet executives who've had exits. Examples:Huiwen Wang (former Meituan co-founder), Hua Su (Kuaishou co-founder). They invest both as LPs in funds and make direct investments.

1.7 Overseas Investment Institutions

Representative firms:

- Sovereign wealth funds: Temasek, Prosperity7 Ventures (Middle Eastern SWF, participated in Zhipu's round at a $3bn valuation in 2024)

- Early-stage firms: Antler (started hosting offline events in China in 2025 to source deals, though early-stage investing in China is extremely challenging—shown by MiraclePlus's track record)

Challenges facing overseas investors making direct investments:

- Deal flow access: Quality deal flow typically circulates within local networks first

- Decision velocity: Foreign institutions' approval processes are generally longer than local funds, reducing competitiveness on hot deals

Summary: In 2025, China's VC market is dominated by RMB funds. USD funds are returning amid FOMO, CVCs are active, PE is waiting for windows, and foreign funds have limited participation.

2. Key Structural Shifts in Recent Years

2.1 RMB Funds vs. USD Funds

China's primary market is now dominated by RMB funds; USD fund share is minimal. However:

- In AI applications and cross-border/global sectors, USD funds still have significant advantages

- The 2025 FOMO comeback proves that USD fund interest never truly disappeared—they were simply waiting for a reason to re-enter

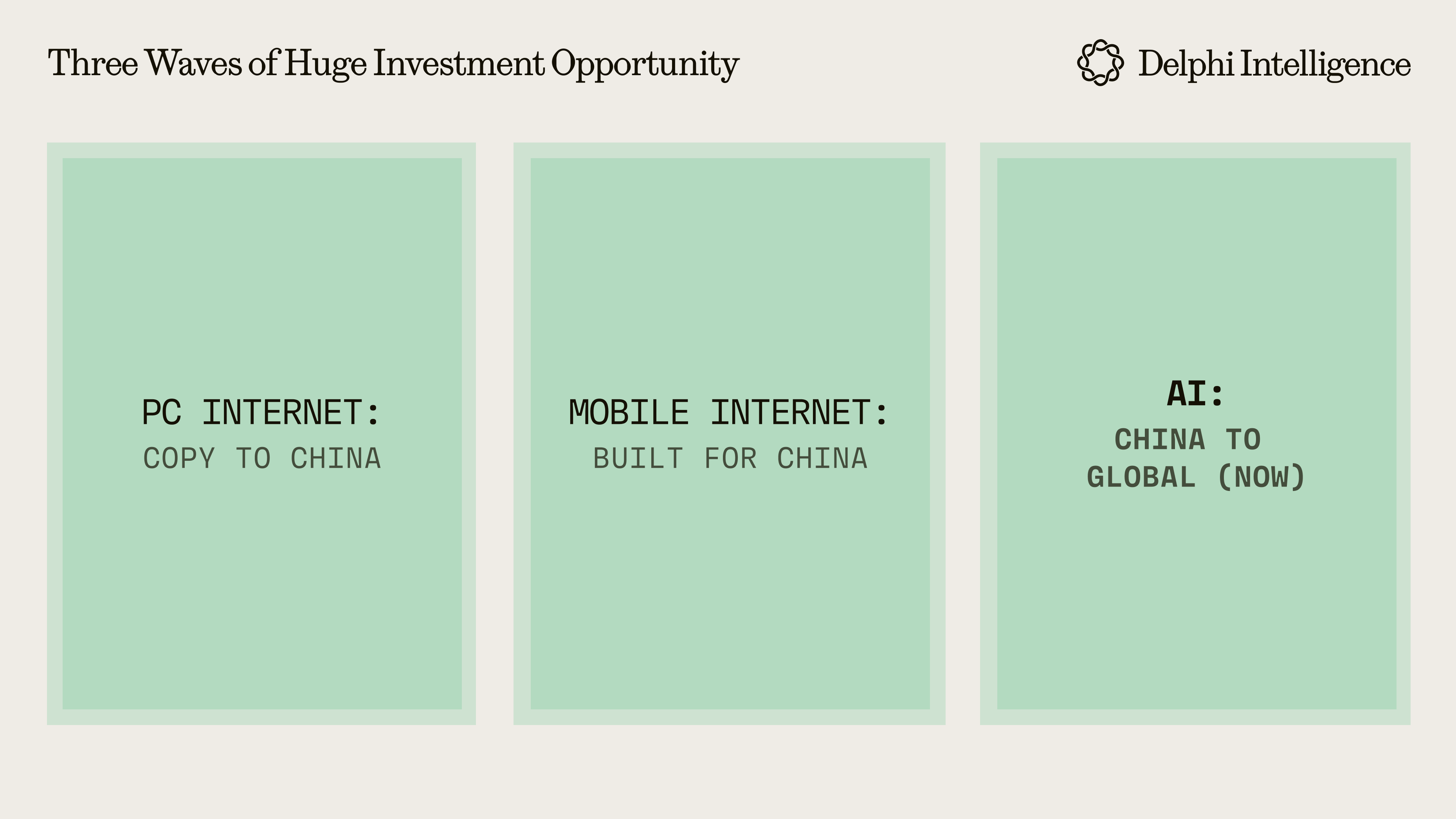

2.2 USD Funds Betting Big on "China-to-Global" AI Startups

The global AI landscape is largely driven by innovation from the U.S. and China: As highlighted in a16z‘s Top 100 Gen AI Consumer Apps report, a significant percentage of leading AI applications are developed in China, and “exported” globally.

In 2025, following the successful release of DeepSeek R1 and Manus, Chinese VCs have gained greater confidence in Chinese AI founders and are investing aggressively. This catalyzed a new entrepreneurial paradigm:

- Founding teams are Chinese (Tsinghua, Peking University, or Big AI Lab backgrounds)

- Targeting global markets from Day 1, not just serving Chinese customers

- Products and GTM strategies oriented overseas

- Leveraging China's engineering talent for lower R&D costs and faster iteration

Why these companies are highly attractive to USD funds:

- Global markets mean larger TAM and clearer exit paths (U.S. IPO/overseas M&A)

- Avoids policy uncertainty inherent to pure-China businesses

- Aligns with USD LP preference for "investing in Chinese teams without Chinese market risk exposure"

- Valuation logic can benchmark against Silicon Valley peers while cost structure is significantly more efficient

For overseas investors: These "China-to-Global" AI companies may be the optimal entry point for foreign capital to participate in China's innovation ecosystem—you're investing in Chinese talent and technical capabilities, but exit paths and market risks align more closely with global tech investment logic.

Additionally, Chinese USD VCs are highly homogeneous and rarely provide differentiated value to portfolio companies. Overseas investors actually may have an opportunity to help portfolio companies with global expansion.

2.3 Significant Deal Flow No Longer Publicly Disclosed

In the U.S., databases like PitchBook cover basic information on the vast majority of VC transactions, providing a relatively complete market picture. In China, such infrastructure barely exists.

- Local databases exist, but data coverage and accuracy fall far short of overseas equivalents

- Many AI projects actively choose to stay low-profile and don't disclose in early stages

What this means:

- Publicly available China VC investment data may only reflect 40-50% of actual market activity

- Real deal flow, valuation intelligence, and sector insights circulate within relationship networks

- If you don't have trusted local partners or information sources, your market picture is severely distorted

Part 2: USD Investment in China

1. Market Evolution

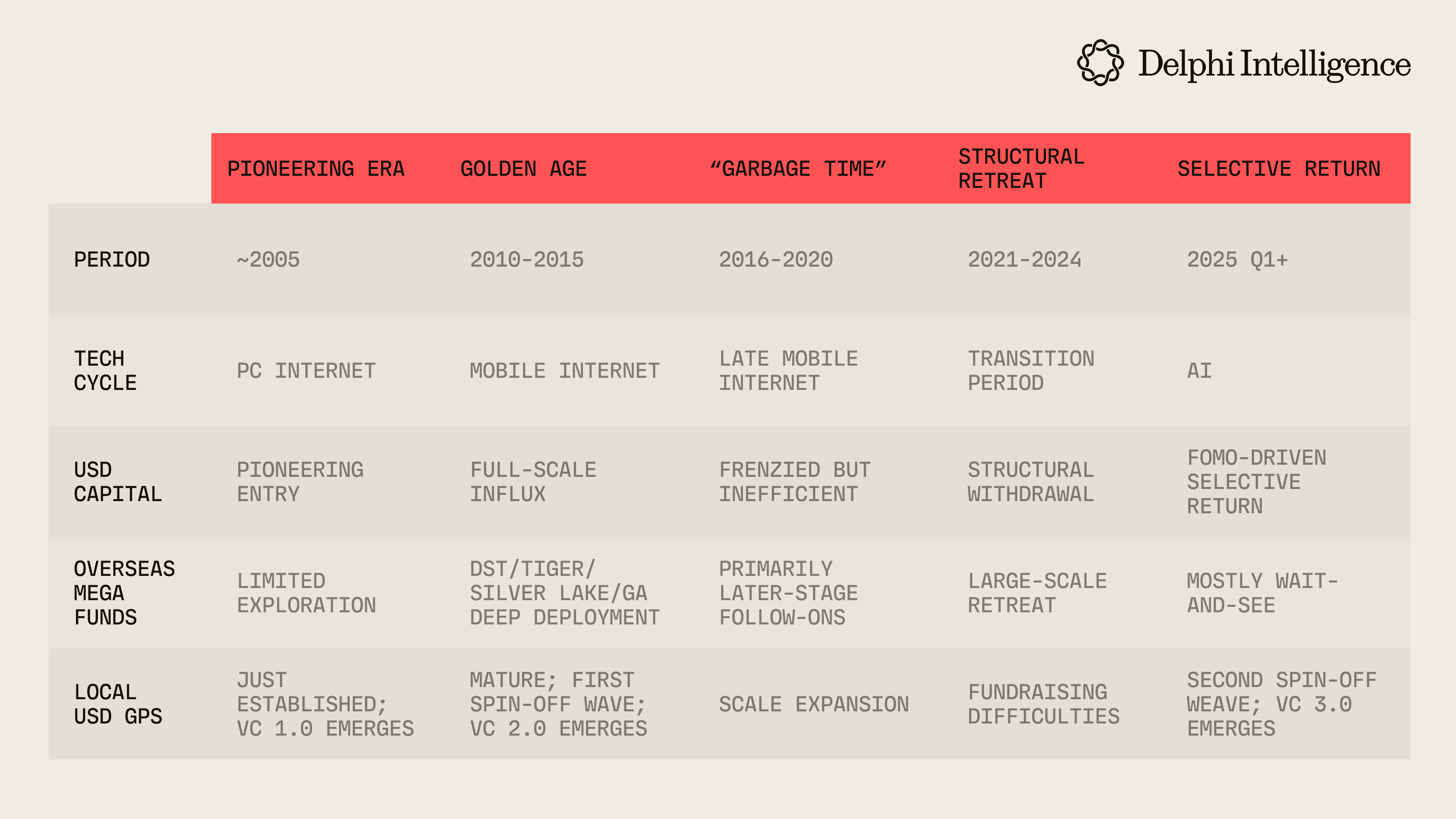

China's USD VC sector has gone through five phases and three waves alongside technology cycles and macro environments:

Phase 1: Pioneering Era, VC 1.0 Born (~2005)

Market environment: China's internet was just emerging; PC internet exploding

Investment themes: search engines, e-commerce, gaming, early mobile value-added services

Key players (also known as VC 1.0): IDG Capital (one of the earliest USD VCs to enter China), Sequoia Capital China (founded 2005)

Characteristics of this generation:

- Partners mostly had returnee backgrounds or foreign investment banking origins

- Investment thesis centered on "Copy from US"—looking for China's Google, Amazon.

Phase 2: Golden Age (2010-2015)—Historic Window, Foreign USD Floods In, VC 2.0 Emerges

Market environment: Mobile internet explosion from 0 to 1; smartphone penetration rising rapidly

Investment themes: Mobile apps, O2O (Meituan/Didi), consumer brands, Fintech, SaaS

Key players:

(1) Local USD GPs had grown more mature

Sequoia, Matrix, IDG and other first-generation VCs harvested significant returns. Early rounds for Meituan, Dianping, Didi, Toutiao were primarily led by local USD GPs.

(2) Top-tier global funds deeply deploy in China

2010–2015: A cohort of the world's premier tech investment institutions systematically went heavy on China for the first time. DST, Tiger Global, SoftBank, Warburg Pincus, Silver Lake, and General Atlantic were all highly active in the China market.

(3) Spin-off wave from top firms; VC 2.0 emerges

This period also catalyzed the "first spin-off wave" among local GPs. Investors from leading funds departed to establish their own GPs.

Phase 3: Superficial Prosperity, Actually "Garbage Time" (2016–2020)

This was a highly deceptive period. On the surface:

- Deal count and volume hit record highs; mega rounds became frequent; unicorn count exploded

- Overseas capital continued flooding in at scale

In retrospect, 2010–2015 was the true "Golden Age" for China internet USD funds. 2016–2020, despite appearing extremely active, was actually "garbage time"—capital flooding in frantically, but virtually no real 0→1 new giants emerged. Mostly bubbles and inefficient deployment. Conversely, this was actually the window for deep tech sector capital deployment.

Phase 4: Structural Retreat (2021–2024)

2021's regulatory storm and escalating U.S.-China geopolitical tensions led to structural withdrawal of USD capital from China market. Local USD GPs faced fundraising difficulties; some small/mid-sized GPs effectively ceased operations.

Phase 5: AI-Driven Selective Return (2025 Q1 to Present); VC 3.0 Emerges

DeepSeek and others rebuilt global confidence in Chinese AI; USD funds returned amid FOMO. Heavy focus on AI capital deployment.

Simultaneously, mirroring the 2015 spin-off wave where core talent from leading VCs departed to establish new GPs, the AI wave has catalyzed new GP formation. Examples: Monolith, Creekstone.

In summary, China's local USD VC landscape has evolved into a VC 1.0, 2.0, 3.0 framework:

2. Key VC Investment Data 2021-2025

Notes:

- As mentioned earlier, significant deal volume in 2024-2025 wasn't publicly disclosed; data only reflects trackable public transactions. Actual deployment is higher.

- Investment data above includes both RMB and USD investments.

- Red highlighting indicates top 8 GPs by deal count each year, reflecting shifts in their deployment cadence over time. (e.g. GGV is less activate in 2025 compared to 2021)

- 2025 overall deal count up 52% YoY, showing "FOMO return”. Green highlighting indicates above average YoY growth

- Investment quantity≠ investment quality—some VCs pursue spray-and-pray, others concentrate on conviction bets.

- For some funds, given FOMO sentiment, 2025 vintage returns may not be optimistic.

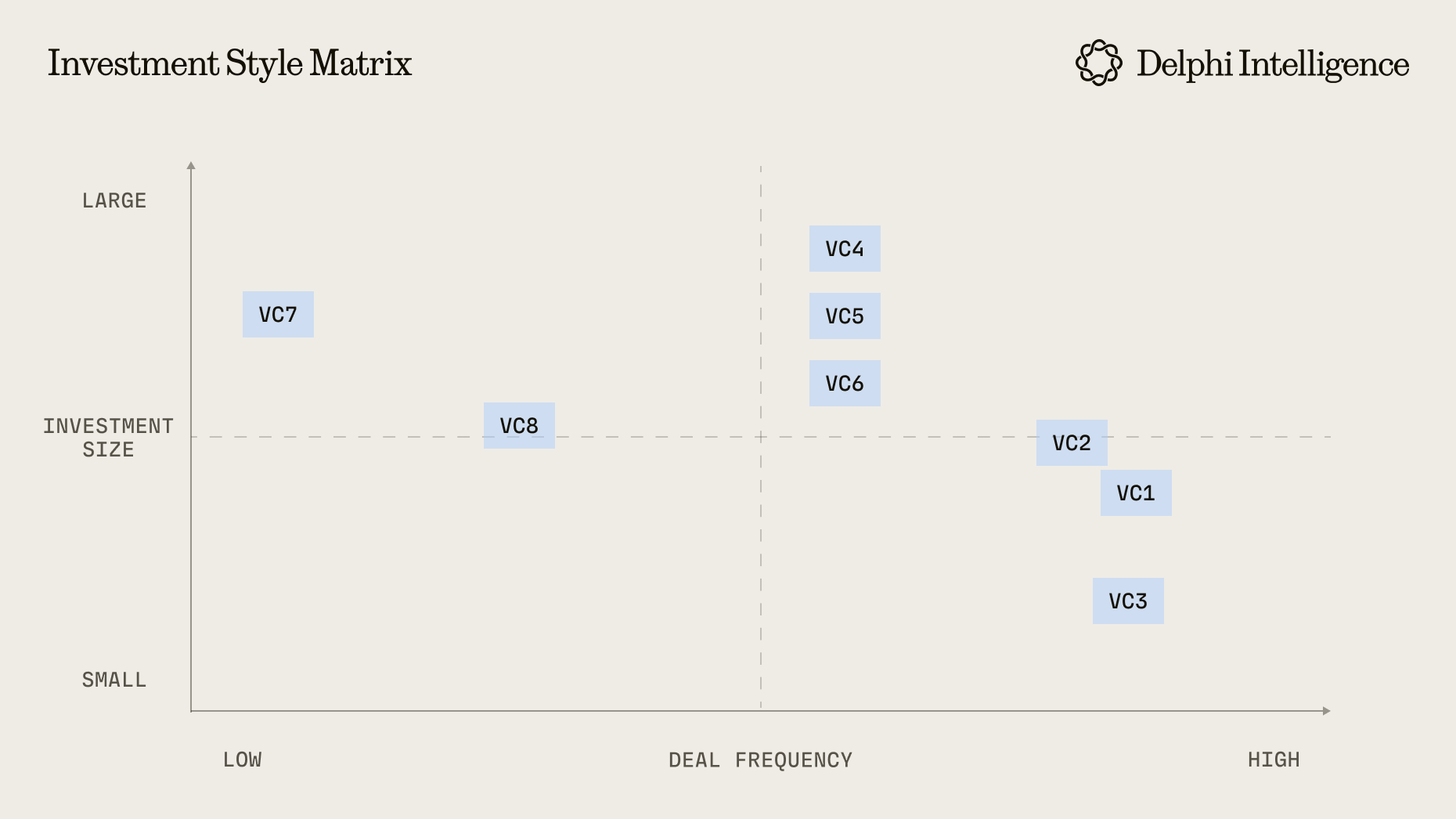

3. Three Investment Styles (AI Investments Only)

Currently, USD VC investment styles for AI deals can be broadly categorized as follows:

Category 1: Aggressive expansion, spray-and-pray: VC1, VC2, VC3

Category 2: Concentrated bets on key sectors: VC4, VC5, VC6

Category 3: Relative selective: VC7, VC8

Note: Actual VC names are not disclosed herein and are anonymized as VC1, VC2, etc.

Institutional FOF investors are welcome to contact us for further discussion.

4. Early-Stage Overheated, Growth-Stage Non-Consensus

Over the past two years, a dominant strategy in China's VC market has been "invest early, invest small". The logic is simple: In the early days of the AI wave, no one knows which direction will win—so cast a wide net, take early positions, and use small checks to buy optionality on future developments.

If a founder's pedigree is strong enough—say, a senior product lead from a ByteDance business unit starting an AI app, or a core DJI engineer launching a hardware company—multiple VCs will compete to issue term sheets before the company even has a product. This competition has pushed seed valuations to wildly irrational levels.

Yet many of these overpriced, hotly-contested deals have exposed serious issues after product launch: such as user growth below expectations, insufficient product differentiation, unclear monetization paths. Once the early-stage halo fades, market enthusiasm for these companies cools rapidly. Follow-on financing becomes extremely difficult.

On the other hand, there's a counterintuitive phenomenon: some projects are not as well-known, or the founders' backgrounds are not as impressive—even if these projects have already built a meaningful user base, they still struggle to raise funding smoothly. This value gap has gradually gained market attention since late 2025—some investors have begun proactively seeking growth-stage companies with ~$10M+ ARR.

Part 3: Active AI Investment Themes

1. Theme Rotation

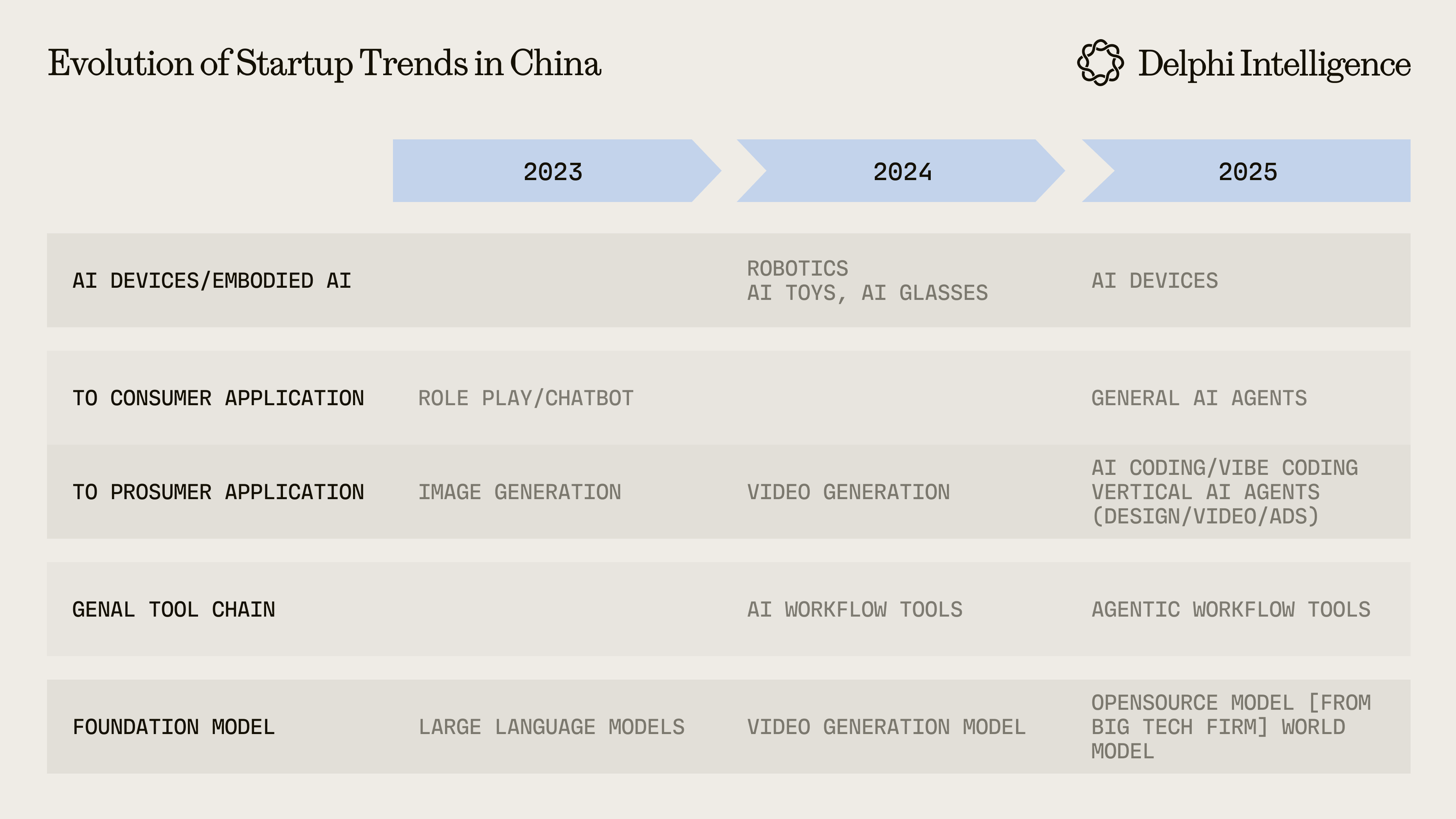

Hot sectors in China AI investing rotate rapidly each year:

2023—Year of Foundation Models: Core themes included Foundation models, AIGC tools

2024—Embodied AI Awakening: Embodied AI/Robotics valuations skyrocketed; leading companies completed multiple rounds within a single year

2025—Agent and Hardware Explosion: AI Agents, AI hardware, AI for Science. Capital began shifting from "investing in models" to "investing in applications and deployment"

2026 (Prediction)—2C Application Scale-up: Many consumer AI applications currently in stealth mode will debut en masse; 2C may become the next major battleground.

2. Sub-Sectors—Software

2.1 Foundation Models

Landscape: Game largely set; entering steady state.

Unlike the U.S. market which continues to see new model labs emerge, China's foundation model competitive landscape has largely stabilized. Leading players are clear; the window for new entrants has essentially closed. Current players fall into four tiers:

- Big Tech in-house: ByteDance (Seed/Doubao), Alibaba (Qwen)

- Local Government-supported: Zhipu AI, Stepfun

- Market-oriented: DeepSeek, Minimax, Moonshot (Kimi)

- Falling behind/marginalized

China-U.S. Differences

- Pricing. In the U.S., represented by ChatGPT and Gemini, strong capabilities command pricing; monetization path is clear. In China, major foundation models feature free public access (for non-commercial use) and open-source.

- Use cases differ. In the U.S., typical ChatGPT use cases are writing emails, coding, research. In China, except for similar use cases, AI has also rapidly penetrated lifestyle services—2C apps can even help users order bubble tea. Chinese AI products are evolving from "tools" to "lifestyle service entry points."

- AI mass adoption may outpace the U.S. The foundation model war during Chinese New Year 2026 accelerated the pace at which ordinary Chinese users use AI.

2.2 Video Generation Models

Landscape: Within Big Tech's strike zone; startups need differentiation to survive

Video generation is one of the hottest technical directions in AI for 2024-2025, but it's also a sector where startups can easily be steamrolled by Big Tech.

Big Tech models are performing extremely well: Kuaishou's Kling was China's first breakout video generation model; ByteDance's Seedance is playing catch-up; Alibaba's Wan is pursuing an open-source strategy.

Startups fall into two categories:

- Launched products with market validation: Vidu, PixVerse, MiniMax Hailuo, HiDream

- Still early-stage, VC-backed: Video Rebirth, Sand AI, Vivix (real-time interactive multimodal)

Video generation model investments carry relatively high standalone risk. Focus on companies building differentiated application scenarios or unique interaction paradigms on top of video generation (e.g., Vivix, backed by IDG & HongShan, RMB 1.3bn valuation).

2.3 3D Generation Models

Landscape: Early stage

3D content generation is less mature than video generation but has significant long-term potential. As downstream use cases in AR/VR, gaming, e-commerce 3D display, digital twins, etc. develop, demand for 3D generation will continue growing. Chinese teams are globally competitive in single-object 3D asset generation.

Chinese teams: Meshy, Vast, deemos

2.4 AI Agents

Landscape: Extremely crowded; products converging

AI Agents are one of 2025's hottest investment themes, but products are highly similar, competition is extremely fierce, and long-term moats are unclear.

Key sub-categories:

- General Agents: e.g., Manus, Genspark

- Coding Agents: e.g., MGX, Trickle, Youware

- Sales/Marketing Agents: Many VC-backed projects; no clear leader has emerged

- Functional Agents: Education, data analytics, etc.

- Agent platforms: Agentic workflow

- Vertical Agents: Finance, legal, healthcare—not particularly vibrant

Currently, the best-performing Agent products are Manus and Genspark. Chinese teams' advantage lies in exceptional engineering execution and product iteration speed. However, the most significant issue with the AI Agent sector currently is: Products are very similar; functionality is highly converging. This means low switching costs, Big Tech can enter anytime, and moats come more from data accumulation and user habits than from technology itself.

2.5 Image & Video AI Applications

Landscape: Chinese teams highly competitive globally.

This is one of the sectors where Chinese AI entrepreneurs have done best at going global. Numerous Chinese team-developed AI image/video tools have already achieved significant user bases and revenue in overseas markets.

Key sub-categories:

- General image generation & design tools/aggregation platforms. Relative mature sector. Some companies have ARR exceeding $10m, with clear commercial validation.

- Video Agents: Following Sora 2's release, Q4 2025 saw very active fundraising for video Agent projects.

- Anime creation tools: Some startups focus on anime-related image and video Agents, targeting very niche markets but performing well. These products benefit from the massive ACG (anime, comics, games) user base in China and Japan. While market size doesn't match general-purpose tools, user stickiness and willingness to pay are both high.

- Image/video generation tools for e-commerce scenarios

- Film production/short drama related: Startups are exploring AI applications in video production workflows. Additionally, AI + short dramas is a classic "China-native scenario"—short dramas themselves are exploding in China and exported globally.

Chinese teams' core advantages:

- China is the world's largest short-video market; teams have deep understanding of video content.

- Image/video tool products are naturally suited for globalization—visual language has no borders

2.6 Consumer AI Applications (2C)

Landscape: Heating up in 2025; teams generally extremely low-profile.

This sector began accelerating in H2 2025, with AI-native entrepreneurs emerging in social, travel, local services, and other directions. More teams remain in stealth mode; expect a wave of debuts in 2026. This is a sector requiring early positioning, but with extremely high information asymmetry currently.

China's structural advantages for 2C AI applications:

- Domestic experience: 1.4 billion population plus the world's most complex commercial ecosystem. China's market scale and scenario diversity provide an extremely fast product validation environment for AI applications.

- Mature infrastructure: AI applications can seamlessly integrate with WeChat Pay/Alipay, food delivery services, enabling closed-loop from "conversation" to "transaction."

- Validate domestically first, then go global—This pathway has been repeatedly proven effective: PDD→Temu, ByteDance→TikTok are successful examples of this logic.

2.7 Voice AI

Landscape: Compared to the U.S., China has fewer voice AI startups, but several directions worth watching.

- AI Podcasts—AI auto-generating podcast content, or converting text to natural conversational audio. Google NotebookLM's success validated demand; Chinese teams are following suit.

- Voice Input—Exploring AI input methods beyond keyboards

- Customer Service/Sales. Chinese-founded startup Retell provides AI voice conversation capabilities for enterprises, with strong traction in overseas markets. ARR has exceeded $40M, making it the benchmark case in this sub-sector.

3. Sub-Sectors—Hardware

3.1 Embodied AI & Humanoid Robots

Landscape: Long-cycle sector; multiple global leaders will emerge from China

Embodied AI may be the direction where Chinese AI entrepreneurs have the greatest structural advantage. This advantage isn't a single point—it's systemic:

- China has the world's most complete robot components supply chain and industrial clusters. For equivalent-spec robot hardware, China's manufacturing costs can be 50-70% lower than the U.S.

- China has abundant engineering talent in robotics and automation, with compensation levels far below Silicon Valley.

The first wave of 2024-2025 investment has already pushed leading company valuations to elevated levels. But the sector is large enough (trillion-dollar market), and new startups continue emerging in 2025-2026. Specifically, there are several categories:

- Brain (Manipulation). Few companies work on this; the industry consensus is that technical approaches haven't converged, and no clear scaling law analogous to LLMs has been discovered.

- Body (motion control). This is currently the most crowded direction; there are already several hundred body-focused companies in the market. Competition is extremely fierce; many companies are building similar humanoid or quadruped robots with insufficient differentiation.

- Core components: e.g., dexterous hands saw very active fundraising in 2025

- Supply chain: Data collection, annotation. Very active investment in 2025

- Companion/home robots

Leading companies at this stage include Zhiyuan Robotics, Unitree, and Galbot, all with valuations reaching multi-billion dollar levels. Some VCs compare embodied AI to the Chinese EV sector—believing this market won't have just one winner, and will ultimately feature several leading companies coexisting. Based on this thesis, some VCs are choosing a "buy the sector" strategy, investing in multiple leading companies simultaneously to ensure they don't miss the winners.

In summary, this is a long-cycle sector—from product to large-scale commercial deployment may require 5-10 years. Along the way, there will be significant bubbles, and many companies will be eliminated through competition. But if you need to choose one direction in China's AI sector with the greatest global comparative advantage for long-term positioning, embodied AI should be at the top of the priority list. Chinese teams' cost structure and supply chain advantages in this sector cannot be replicated by U.S. teams in the near term. But patience is required—this is not an 18-month exit sector.

3.2 AI-Powered Hardware Devices

Landscape: A diverse category of hardware with varying upside potential.

AI hardware was relatively quiet in previous years, without many exciting startups or products. But entering 2025, this direction suddenly became one of the hottest sectors in China's startup investment market. The catalyst for change was Plaud, significantly boosting market confidence: Plaud, an AI recording pen/AI Pin product, entered the global market with AI recording + real-time transcription + intelligent summarization, achieved $100m+ ARR in 2025.

Currently active AI hardware sub-directions include:

- Always-On products: e.g., Looki, exploring hardware where AI is always online, continuously perceiving the environment.

- AI Recording devices—After Plaud opened this category, more teams followed, exploring AI recording hardware in different forms (pins, pens, etc.)

- AI Glasses: Inspired by Meta Ray-Ban, Chinese teams quickly followed suit

- AI Toys: AI + children's education/companionship is a market which multiple startups are exploring.

- AI Home device: Embedding AI capabilities into home scenarios

Note: Other Hardware

Beyond the mainstream AI hardware above, the following may not be directly AI-related but benefit from the same supply chain advantages and cross-border infrastructure:

- 3D Printing/maker: inspired by Bambu Lab's success, companies like Nestwork and Makera are expanding into global markets

- Exoskeletons: Hypershell and others are making consumer-grade exoskeleton products, extending from industrial assistance scenarios to consumer scenarios (walking assistance, athletic enhancement, outdoor adventure).

- Elderly care: AI camera and sensor solutions targeting growing aging market

- Outdoor cleaning robots: e.g. snow removal robots, pool cleaning robot

4. Other Emerging Themes

4.1 Agent Infrastructure

Landscape: New infrastructure layer forming around the Agent economy.

Unlike the U.S. where AI infrastructure investment is very active (databases, model deployment, evaluation tools, observability platforms, etc.), China's AI technical infrastructure investment isn't particularly active. Instead, commercial infrastructure—especially payments— is a more activate sector.

The logic is simple: As AI Agents proliferate, entirely new infrastructure needs are emerging. Whoever can become "Alipay for the Agent economy" or "Stripe for the Agent economy" will capture a massive opportunity. Multiple startups have already raised funding, exploring infrastructure that provides payment and transaction capabilities for Agents.

4.2 AI for Science

Landscape: Long cycle, high barriers, high return potential

China has abundant talent in chemistry, materials, biology, and other fundamental sciences. Additionally, the massive scale of manufacturing provides rich application scenarios for AI scientific computing (new materials, new processes, etc.). This is a sector suitable for patient investors with scientific background understanding.

Conclusion

China has numerous AI sectors with rapidly rotating hot themes. Investors cannot cover every direction. Recommend using a simple screening criterion to filter noise:

Invest in China's supply chain and engineering talent advantages, but aim to have investment exposure to global market revenue and exit paths.

By this standard, AI hardware, embodied AI supply chain, and image/video applications with proven global capabilities may be the most natural entry points for overseas capital.

.png)