We did a Delphi & friends China trip over the last two weeks. Valuations in AI, robotics and deep tech have been accelerating materially, meriting greater caution - but it still feels closer to the 4th or the 5th inning with room to run.

Note: my colleague Jose recently wrote his own takeaways here. While we wrote our essays separately, there is some overlap. However, there are enough differences where I believe posting mine is also valuable. It’s worth emphasizing that the takeaways are relative to the quite high expectations at the start of the trip, not an absolute stance on the investability of either hardware or software. We will continue actively looking at investments in both areas.

Lastly, I was happy to get the Delphi team on the ground. More people should visit China and form their own views from first person exchange.

A large thanks to the many teams who were hospital hosts during our stay.

The Upswing

Thirteen months ago, China was uninvestible and DeepSeek was not a household name. Flash forward and Zhipu is trading at ~US$35b, Minimax has overtaken Baidu in market cap, and every humanoid company in China is racing for the IPO window. Early stage rounds are not immune: AI adjacent startups are now regularly receiving multiple up rounds per year- accelerating towards parity with their US counterparts despite shallower private growth and public capital markets.

It's surprising to see how quickly this has happened.

MoonShot AI (the AI lab behind Kimi) was still valued at US$4 billion in December, before jumping to US$6b in January, US$10b in February, and is now raising at US$18b in March. While US$4b in December was clearly undervalued relative to traction and talent, the recent inflection has clearly been aided by comparisons to white hot listed peers, the staying power of which - post lock-ups - is questionable.

I remain bullish on Chinese tech because of the density of human capital, the considerable investment by the state in science, basic research, and deep technologies as well as the (still) relative underweighting of global capital. However, the pace of valuation acceleration in tech - underpinned by government policy and retail enthusiasm versus financial fundamentals - provide reason for greater caution.

If you were putting money to work in early stage AI twelve months ago, you are likely sitting on ~3-5x gains after two up rounds. The next leg of the cycle will be about alpha as opposed to beta.

Sector Specific

Perhaps expectedly, I also left the trip modestly more bullish on Chinese hardware and deep tech and more circumspect on Chinese software and Open Source AI labs, though there are bright spots.

Hardware

Our meetings with dozens of startups and VCs cemented just how hard it will be for non-Chinese supply-chains to compete. Entrepreneurs we spoke with mentioned up to 70% of inputs would be sourced from the Great Bay Area (spanning Shenzhen, Guangzhou, HK, Macau +) and close to 100% from China itself. This allows for product iteration cycles in days as opposed to months. Outside of obvious supply chain advantages, the increasingly abundant electricity, the public subsidies, and the obviously low 7:1 exchange rate, combine to make it extremely difficult for other regions to compete. The "reindustrialization of the west" cannot happen without heavy money printing, inflation, and currency devaluation; a confluence unpleasant enough to succumb to any single election cycle.

As the AI revolution increasingly allows energy to be transformed into intelligence, complements like hardware excellence appear well-positioned. Within China's cutthroat hardware ecosystem, founders outperforming are not the computer sci grads or the algorithmic whisperers but the electrical and mechanical engineers spinning out of shops like DJI and Insta 360.

In a world where AI commoditizes software, atoms become the bottleneck. To me, this is relatively bullish for China, whose economy relative to the west or India has a much greater degree of manufacturing relative to services.

Consumer Hardware

DJI is the unquestioned talent hub for consumer hardware, followed by Insta 360 and, to a lesser extent, Huawei. The low hanging fruit is for Chinese founders to reimagine existing appliances in the age of AI - from automated lawnmowers to self-navigating wheelchairs to better, cheaper vacuum cleaners. These verticals are already scaling into the hundreds of millions in topline, profitably.

However, the more interesting companies are those integrating hardware and software to create fundamentally novel markets. These markets often start out looking like a niche - whether DJI with drones or Bambu Labs with 3D printing - but ultimately grow into dominant category leaders much larger than either the entrepreneur or investors initially underwrote.

Despite sanctions, DJI allegedly does ~US$10b in topline and US$3b in profits. One source told us Bambu labs will reportedly pass US$1b in profits growing 60% YoY (unverified). These companies are monsters: built atop novel tech stacks with rapid iteration cycles that escape the brutal competition of China's other "me too" hardware products which are so often a race to the bottom.

While the world's attention remains captured by humanoids, perhaps the next understated category destined to surprise is actually human enhancement: human-centric exoskeletons or mobility devices which penetrate everyday use cases to make human life more convenient.

Another hot category is ambient computing. From glasses to pins to phones to camera networks, a host of form factors are competing to power the context thirsty agents increasingly set to govern our daily lives. While the final form factor remains elusive, their origins almost certainly lie in Shenzhen.

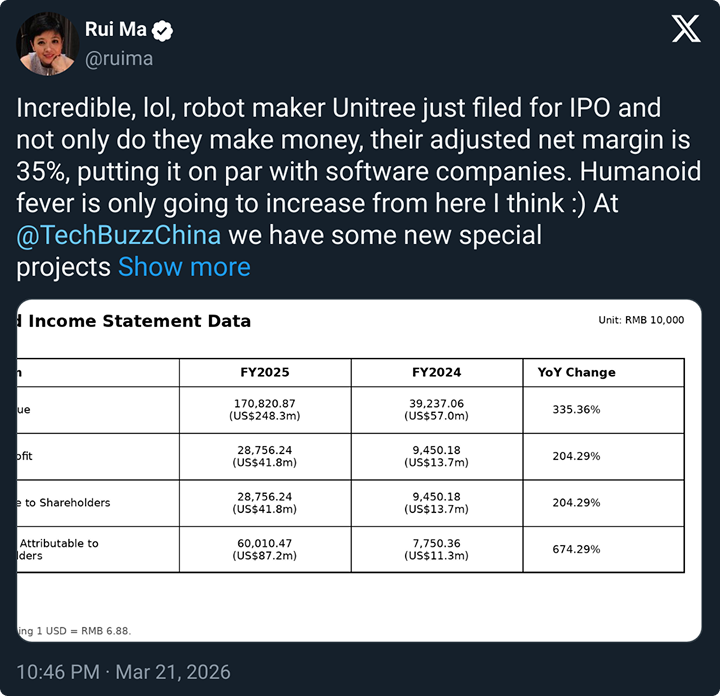

Humanoids

From Galbot to Agibot to Unitree to EngineAI and more, the market for humanoids in China is undoubtedly crowded, enthusiasm seemingly surpassing actual utility.

That being said, the financial profile of some of the leading companies is surprisingly healthy:

Incrementally, the dozens of VCs and entrepreneurs we spoke with were extremeely confident in China's positioning. ~70% global share was floated consistently.

Looking at the trajectory of the drone market, the EV market, the phone market, and other consumer electronics, perhaps this is unsurprising. Though like EVs and phones, the product positioning, domestic competition, and rising trade barriers may turn 70% of market share into only ~30% of market profits. Then again, this time may prove different.

What is clear, however, is that China's demographic challenges, its dense supplier networks, its energy subsidies, and its greater readiness to deploy (with less legal / regulatory blockers), make it the likely volume leader in what is almost certainly going to be one of the world's largest markets. Faster deployments in greater numbers may also kick start a data flywheel which overcomes China's current algorithmic and chip deficiencies.

The crowded field of contenders is now in a race to list. The names will almost certainly trade up on listing, but whether there is enough liquidity to avoid a host of peers and unlocks remains in question. While industrial-focused humanoids raise billions and race to IPO, early stage VCs are increasingly betting on robots for the home - whether in the humanoid form factor or something cuter - like domestic pets.

Deep Tech

Another area of relative bullishness is China's deep tech ecosystem. This is often difficult for off-shore capital to back, due to both US and Chinese regulations and price distortions from less return-sensitive, state-tied pockets of RMB capital. These industries include energy, materials, semiconductor supply-chains and much more. On all three fronts, China is making impressive strides.

I will not dive into every segment, but Tanner Greer's recent substack post covers it well. China is pouring immense resources into scientific research. It's universities now top global rankings. It’s researchers the most published. It’s trajectory undeniable.

The flow through to industry is already evident. Power generation across renewables and nuclear is well covered, not to mention battery giants like CATL and BYD. In semiconductors, several industry veterans told us that China had almost completely caught up with the exception of EUV supply chains which is 1) to be fair, a big mountain to climb and 2) may be overstating other challenges to ramping up fab production in frontier memory and logic, but remains impressive given the pace of catchup. In many subfields of next-gen materials, China's research is now leading.

The implications of this basic research push for future industrial competition should be obvious:

"In many areas of science the dominance is total: for example, ten of the most productive research institutions in the fields of nanoscale material manufacturing, photonic sensors, chemical coating, drone operations, automated swarms, and undersea communications are Chinese. The number is nine out of ten for work on supercapacitors, advanced composite materials, inertial navigation systems, and satellite positioning, eight out of ten in advanced optical communications, advanced radiofrequency communications, and new chemical coatings, and seven out of ten for directed energy technologies, nuclear engineering, and nuclear waste treatment."

For a host of reasons ranging from regulations and capital controls, to price distortions from state-tied strategic capital, to general euphoria in China within sectors aligned with policy support, these sectors - while advancing quickly - remain difficult for private market participants to access. However, they will undoubtedly underpin other, more commercial industrial applications in the future and remain a key source of China's growing competitiveness.

Software

The pace set by the big US labs is not slowing down. The fundraising colossal. The revenue ramps unprecedented. The capex ungodly. As long as the scaling laws continue, the US is running the right playbook.

This makes like more difficult for open source labs and also poses risks at the application layer globally.

The financial profile of Chinese labs is paltry in comparison - scoring tens of millions in ARR as opposed to tens of billions for their US counterparts with only ~1 order of magnitude separating the valuations.

I have never been more bullish on the utilization of open source software and agentic networks, and yet remain uncertain as to their ultimate value capture. At this time, the majority of profits seem likely to emerge from frontier-level capabilities; everything else trending towards the cost of electricity.

Without a doubt, the #1 AI talent pool in China is Bytedance. In consumer AI applications, particularly those with video, ex-Bytedance PMs and AI researchers are some of the best positioned founders on earth. They will undoubtedly build some of the largest companies of the AI era.

Yet, they are also racing against the US labs themselves, building companies run by agents - often rented from the most performant labs (Anthropic) for their highest value use cases. The concern is that many of these startups - in the US and China - end up renting their best employees from their competition.

On the other hand, the open source ecosystem is evolving rapidly; agentic swarms compounding at the rate of natural language prompts. Perhaps no developer community globally has bought in to the OpenClaw craze on the scale of China. Every weekend, I get notifications for Claw events attended by hundreds of indie hackers and prospective founders. Just today, a top early stage VC in China told me they are seeing a material upleveling of the quality of A2A startups in just the past couple of weeks alone.

The seeds of a new agentic economy are being built, and its hard not to see a large swath of its leading participants emerging from China.

Chinese Founders

During our trip, my colleague Jose noted that China has an extreme density of engineering talent but a smaller ratio of true outlier "founders." In many ways, this is cliche but true. The Chinese system does reward excellence in conforming to a specific path, making it less legible to VCs sifting for outlier "founder" traits. Despite the breadth of extremely high IQ, highly technical engineers, the Chinese system produces less "weirdos;" the character traits we in the west have identified as most likely to build trillion dollar companies.

On the flip side, I can't help but think many western VCs try too hard to fit Chinese founders into their archetypes derived primarily from a US cohort. The truth is that the cost of being an outlier in China is higher than in the liberal west: both culturally and in terms of the darwinian meritocratic sorting of the system. A few tens of points on the Gao Kao can dramatically impact one's life trajectory and so even small deviations within such a competitive environment come with elevated risks compared with cultures that prize individuality and failure.

It's true. It is often harder to spot the true outliers in China's tech talent network because the profiles on paper are often lower in variance, but perhaps the answer is less in expecting the pool to conform to your existing archetype as opposed to requiring a different, more sensitive lens to uncover them.

This is particularly hard with a language barrier. At many dinners, the environment is loud with multiple conversations ongoing simultaneously, and western VCs expect founders to sell a grand vision in their non-native language. As someone who often attends dinners in Mandarin, I'm quite cognizant of how limiting it is to express myself.

Looking around at the tech ecosystem, it’s clear something is working even if its happening at a more systemic or incrementally compounding level than the familiar "hero's journey". (And then again, there is increasingly more of that.)

So, I’m of dual mind. Relative to the technical talent pool, there are fewer legible outliers and less, true 0 to 1 companies so far. But at the same time, the outliers within the Chinese tech ecosystem clearly exist, perhaps we just need to learn to use a different lens.

Macro

The macro is tricky. On the one hand, Chinese markets remain undervalued relative to global peers and policy makers are actively working on using equity markets as a store-of-wealth inflation lever to combat the ongoing real-estate collapse. This should give Chinese markets a floor in the years ahead. The long-short equity shops we spoke with remain bullish for the next 18-24 months (at this time), given the tailwinds.

However, there are pockets - like the public model companies or domestic semiconductor names - which are clearly in a bubble. There were also whispers of questionable interventions by market makers for small cap names in Hong Kong, not too dissimilar from crypto shenanigans.

Overall, the cycle still has legs, but their are clearly pockets of froth and aping the wrong ones will likely prove costly.

The K-shaped economy is also very real. Consumers in 3rd tier cities are still hurting. According to my informal conversations with small business owners, their sales have not bottomed yet. 2026 is not better than 2025. The deflationary slump is still ongoing and a meaningful boost to equity markets by policy makers is perhaps the most palatable way to combat that domestically.

However, the most recent regulatory guidance aims at driving more of those equity gains to onshore investors and generating greater domestic tax revenues, perhaps a necessary nudge looking at the fiscal situation of many local governments but might make foreign capital more hesitant. The guidance should cool, not freeze what has become a hot market.

In terms of global flows, the Middle Easterners have replaced the Americans at the Four Seasons in Shanghai. European family office capital is trickling back for China tech tours. And perhaps the #1 bonding experience between our American cohort and our Chinese counterparts was "how cooked Europe is."

Some memes are universal.

Conclusion

In short, this latest visit provided more questions than answers to the unending enigma that is China. I left more convinced than ever about China's manufacturing dominance, yet increasingly worried what geopolitical opposition will mean for its economic model. More convinced than ever in the role of open source models and agents, yet unsure of the value capture. More convinced than ever that China has some of the most elite AI and robotics engineering talent on earth, yet still has room to improve in cultivating the outliers most likely to unleash it.

There are only two markets with a vertically integrated AI stack: the US and China. Both are poised to accelerate faster than their technological dependents at this point in the S curve. However, the valuation gap which existed between the two ecosystems in only the last six months has closed considerably. China tech is no longer a "no brainer" valuation wise but has become a market with pockets of froth and pockets of reasonable value just like most others.

Given the policy support and general underweighting in global indices, I suspect the cycle still has legs, but we are clearly no longer at a cyclical trough. The game is getting more micro once again.

.png)