Humanoids Part 1: Sizing the Profit Pools

"When I see a bubble forming, I rush in to buy, adding fuel to the fire.”

— George Soros

Investing in humanoids today is treacherous because it is so obvious. We are clearly on a trajectory where productivity is decoupled from demographics (Edge of Automation): where intelligence will jump from the data center to the factory; from the world of digits into the world of atoms.

The path is so plainly lit that no investment manager can be construed as contrarian in seeking allocation. Many of the expectations have been priced in or are outrunning the near-term realities of penetration. The explosion in valuations and successive funding rounds are tell tale signs to be wary. A stall in enthusiasm would require investor patience for players to grow into these accelerating valuations.

And yet, the writing is on the wall: this market is going to be massive. The capabilities will increase, the costs will decrease, and the long-term ROI for customers is obvious.

The tasks which an AI can complete continue doubling every 7 months. Investments in multimodal capabilities march on to the tune of hundreds of billions. The cost curves of the "electric stack" (Packy) plow downwards. And the base line of it all - energy - appears on a path towards abundance, poised to cut us loose from the hydro-carbon death grip in the decades ahead (Dwarkesh).

By 2050, there will almost certainly be tens of millions of humanoids globally, if not hundreds of millions or even billions.

However, functional humanoids at scale still retain material challenges. Leading AI researchers have still not not cracked multimodal reasoning, let alone embodied intelligence. Simulations are helpful, but they are not enough. Robotics data remains scarce, and the best models too large to fit on-device. The hands still lack the dexterity for many use cases. The components are still too expensive, and scaling up production will take time and substantial investment. All of this before even the inevitable political blowback from a concerned labor force and the ensuring regulatory overreach likely to follow in its wake.

And still, the race for AGI is attracting hundreds of billions annually in investment. Should embodied AI, which arguably expands this TAM by an order of magnitude, not command correspondingly large infusions?

Global labor is sized in the tens of trillions. The long-term ROI on humanoids in many of these domains is obvious, not to mention new markets which will inevitably emerge as costs decrease and capabilities increase. The investments will come.

However, these investments will not take place in a vacuum but atop a complex and shifting geopolitical stage. The US and China cannot possibly hope to truly "decouple" but both are racing to avoid strategic dependencies on their rival superpower. The US retains its lead at the frontier of AI: the chips and datacenter buildout fueling the brains behind the coming humanoid swarms, while China's dominate grip on rare-earth minerals, manufacturing supply chains, and a massive energy build out, position it well in the race for the "technological threshold" (Edge of Automation).

Both will be racing to reduce these dependencies: China investing hundreds of billions in the monumental lift of domesticating the entire semi's value chain, while the US's lift may prove even larger: reshoring the manufacturing processes it spent the last century outsourcing; slowly relearning how to build the machines that build the machines.

The implications for rates amidst an already stretched US fiscal situation are worth consideration and are clearly tied to Bessent's stablecoin embrace, Trump's hammering of Jerome Powell on rates, and Miran’s ascension to Fed Governor. Perhaps the race for cybernoid supremacy will not be decided in Washington or Beijing or even by the neuro-divergent enclaves in Silicon Valley and Shenzhen but by those ever-pesky bond vigilantes.

The humanoid race touches all of the great themes of the 21st century: technology, great power politics, artificial intelligence, reindustrialization, and macro policy.

We hope this four part series can help guide you through these treacherous waters:

- Humanoids: Sizing the Profit Pools

- Software: Mapping the Brains

- Hardware: Real Men Have Fabs

- Integrators: The Race to Orchestrate an Automated Labor Force

In short, I believe we are currently in a bubble for humanoids. Based on the size of the opportunity, I believe this bubble will get substantially larger, especially given how narrow the door is for exposure. I believe the largest companies and nations will consider this race "existential". I believe bubbles tend to be good long-term, laying the infrastructure necessary for an ensuing application wave. I believe money can be made investing smartly within a bubble: going in early or allocating smartly within the value-chain. I believe we will see a Gartner style correction in sentiment in the years ahead as individuals realize the bottlenecks and timelines may stretch out compared with today's elevated expectations. And yet, I believe that the companies which are raising now and have the firepower to ride through a pending correction may end up being some of the largest companies in history by the late 2030s and 2040s and that investors will increasingly looking to "pull forward the future" given the acceleration in AI.

In short, it is a bubble. And given the size of the opportunity, it is one that no investor has the luxury of side-stepping.

Sizing The Profit Pools

The humanoid value chain is complex.

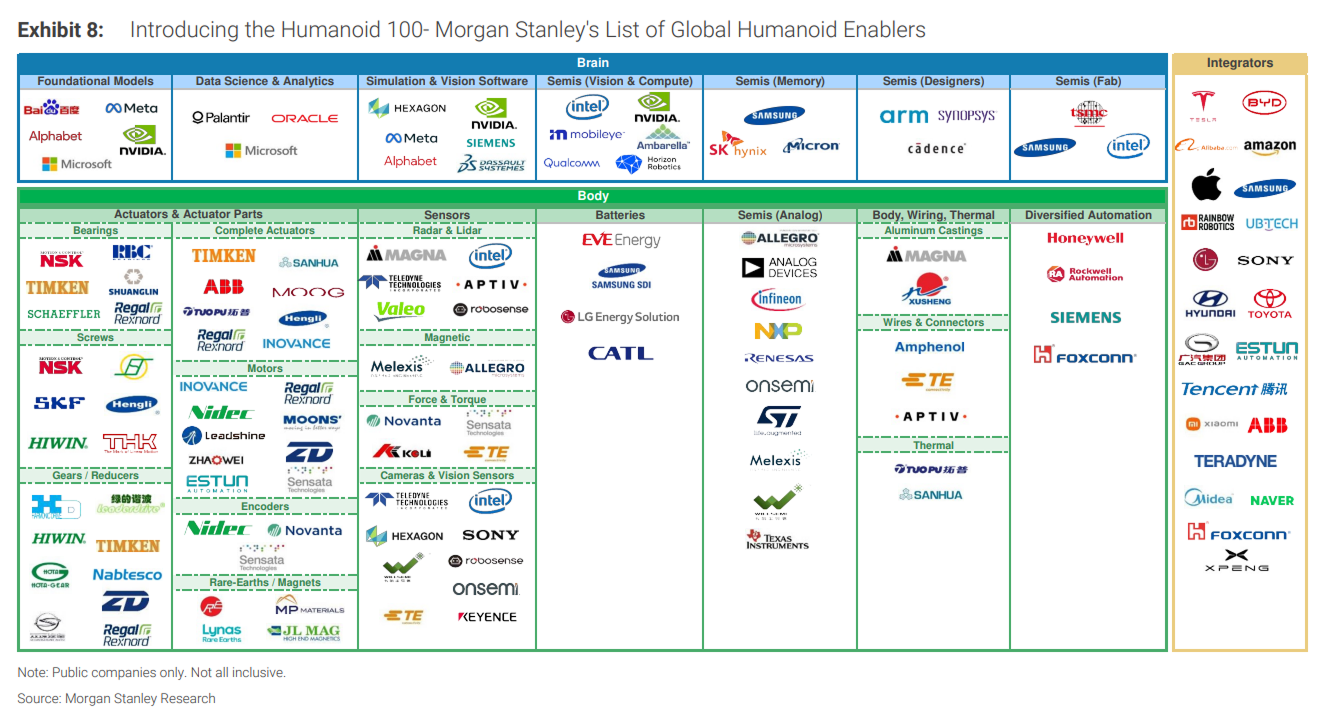

In their humanoid value chain report, Morgan Stanley did a fantastic job of mapping out many key segments in the value chain. However, as equity analysts, they were naturally focused on the public markets.

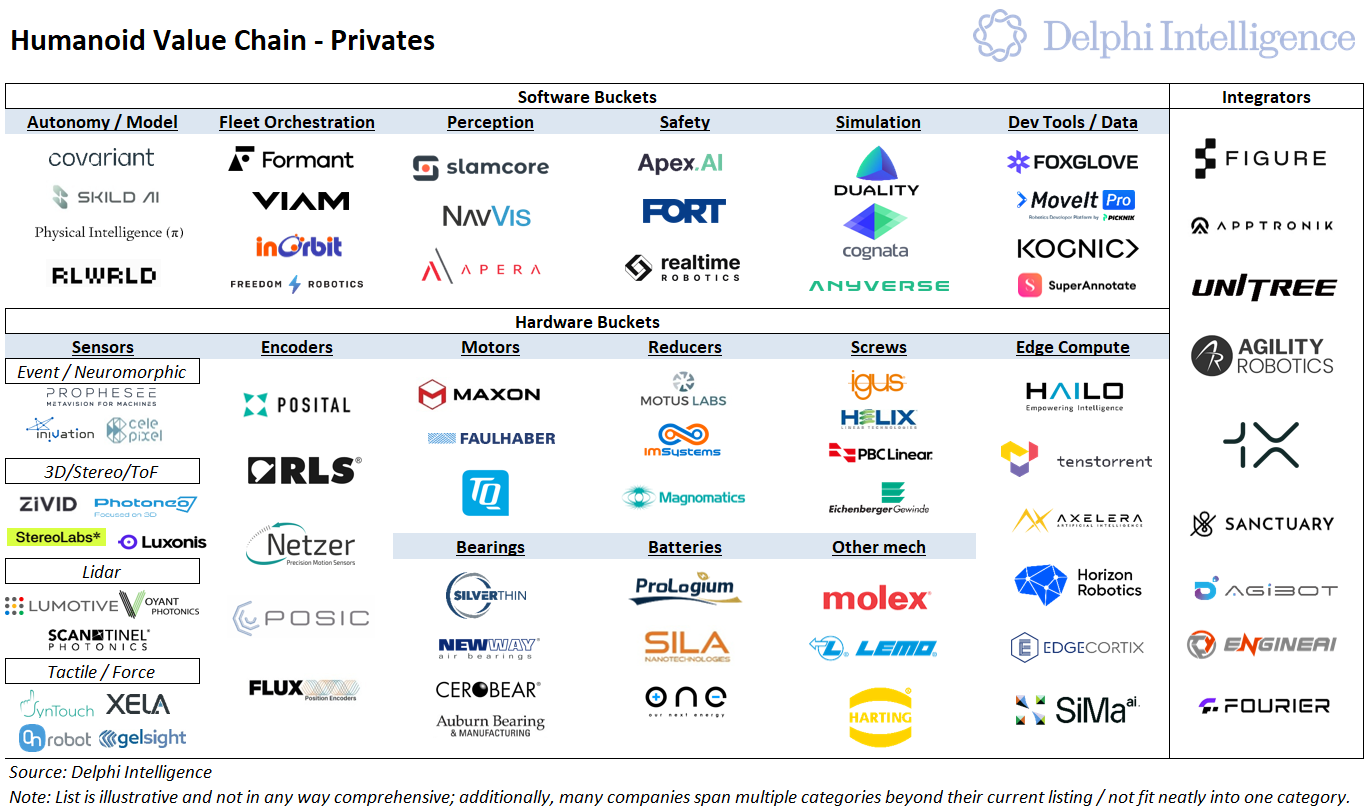

As a private market investor, I wanted a similar map focused on emerging private players in each category.

(Please note the above graphic is an iterative work-in-progress and will evolve with this series as I learn more about each segment of the value chain and the players I’m most excited about)

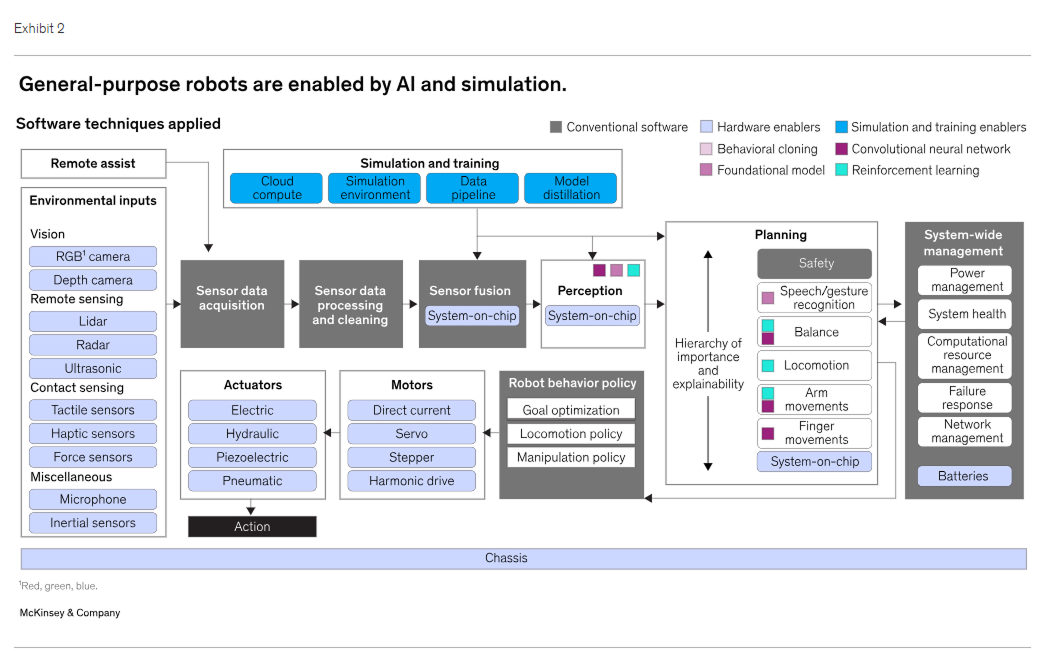

The below graphic from McKinsey provides a solid high-level overview of how many of these key pieces fit together:

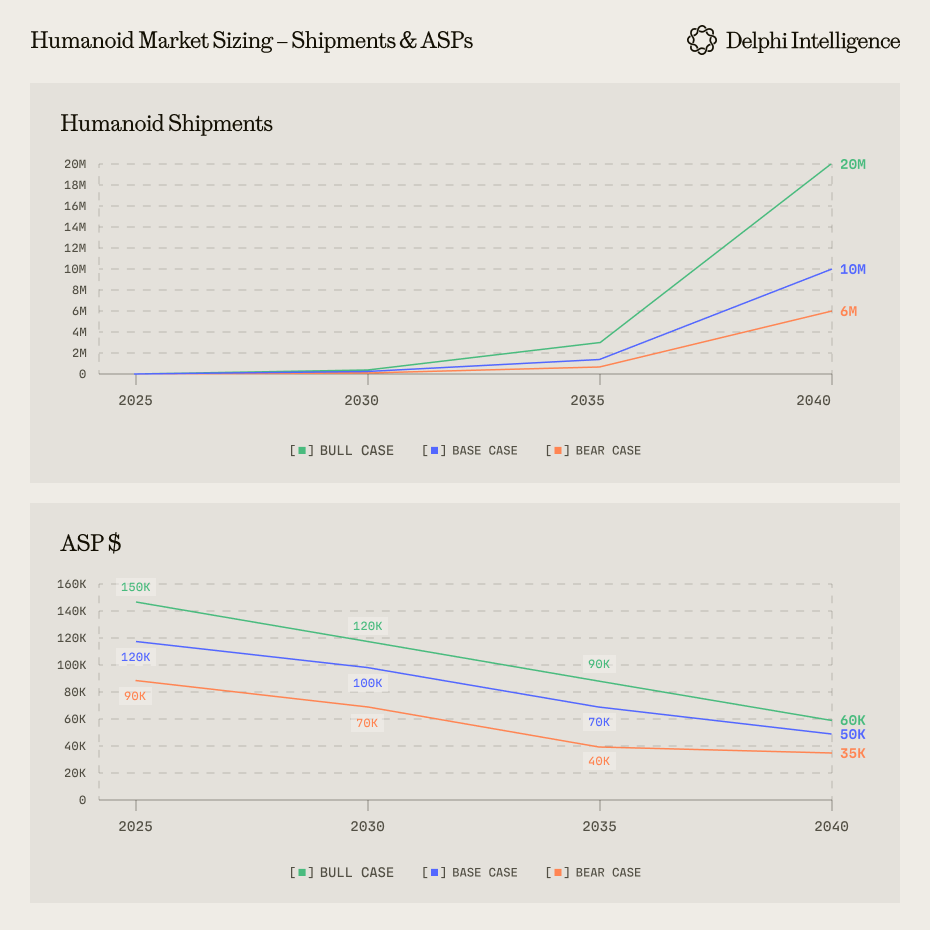

As the value chain is quite broad, we built our own market projections to forecast humanoid shipments by 2040 and break down the corresponding profit pools within the value chain to better prioritize our efforts of where to hunt.

Note, given the speculative nature of the exercise, these estimates are low confidence and span multiple scenarios, projected using five year increments through 2040. However, they are likely directionally correct and helpful in ballparking potential spend.

Momentum only really begins ramping in the mid 2030s and much of the expected growth (i.e. the global inflection) occurs beyond the projection period. In the 2030s, investors will be underwriting accordingly and pulling forward an inflection in future growth.

.png)

In our base case, the ASP drops to US$70k by 2035 and US$50k by 2040. Note this is a global figure. The US (projected at ~25% of global production) would likely be priced at a relative premium while China, as the likely cost leader, would have a greater volume share (~45%) but at lower ASPs. The remainder of the market is expected to be shared between Japan, Korea, Germany, and RoW.

At an average price point of US$50k and an ~8 year life span, the ROI in many of the early use cases - logistics, construction, manufacturing, hospital services, etc - becomes very compelling vs. human labor costs, particularly when considering turnover and effective hourly rate. If the capabilities are there, then demand is likely to outstrip supply in many use cases. Many leading incumbents will also "dog-food" their own humanoids: Optimus operating within Tesla's factories being the easiest example, but in-house robots or partners with meaningful minority interest will clearly be ramping within Amazon warehouses, BYD factories, Japanese conglomerates and beyond.

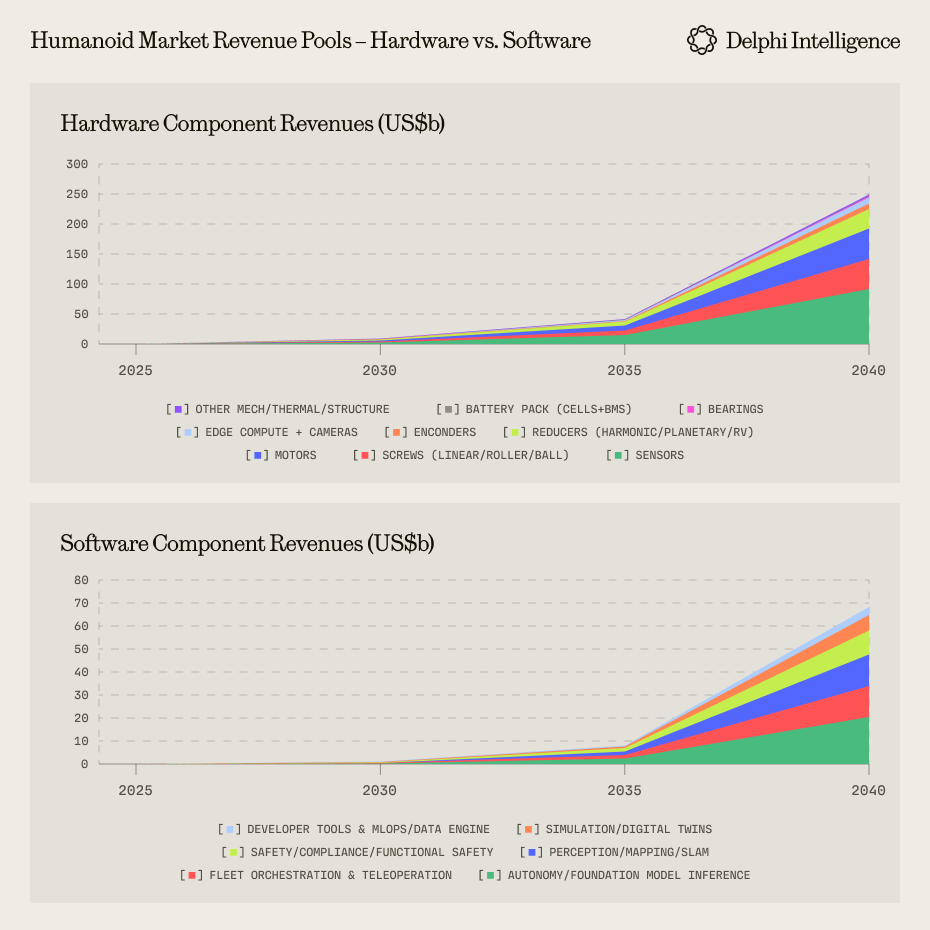

Within the OEM-enabling segment of the value chain, the majority of revenues by 2040 are expected to be from hardware:

.png)

Under hardware, we divided further into nine core categories. Within software, we broke out six:

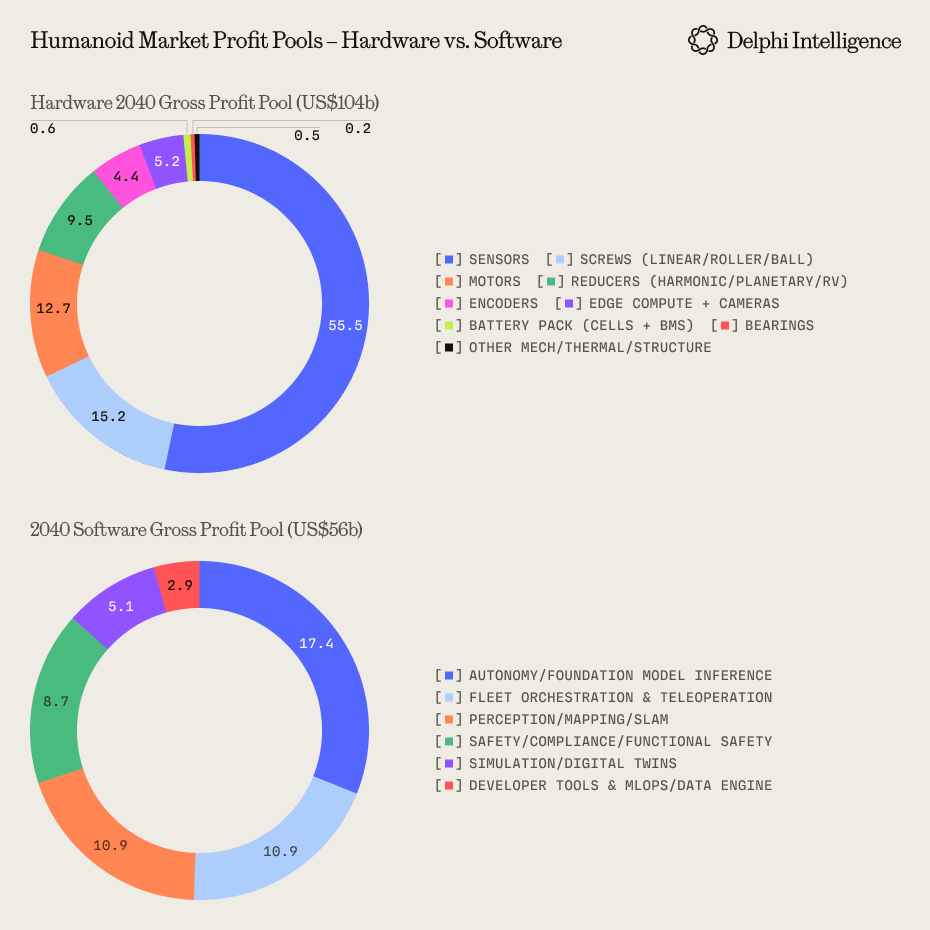

Software is expected to have higher gross margins than hardware but the aggregate profit pools will still be smaller in 2040. After estimating gross margins of the various buckets in 2040, we arrived at the following gross profit pools to help us decide how to best allocate our time across the value chain (again, rough estimates):

Based on the above analysis, the implied profit pool of the OEMs is the most sizable, but within the value chain: sensors, screws, motors, inference, fleet orchestration, perception, and safety are all expected to be ~US$10b+ markets by 2040.

Some may be surprised to find hardware profit pools outstripping software, so I will provide a few caveats.

- Some of the software value is bundled within the sizable OEM profit pool

- By 2040, the industry will be in the middle of an inflection. As volumes ramp, standards arise on the hardware side and commodification will drive margins lower while OEM leaders separate from the pack and scale volumes and leverage over suppliers. I suspect relative value capture will skew more OEM / software the further the industry matures.

However, near-term, components are a favorable hunting ground as have clear tailwinds from humanoids, with an ability to supply multiple OEMs (amidst an uncertain and highly competitive race), while often retaining exposure to other, more established sectors, which provide some protection to the downside.

MARKET STRUCTURE

The value chain for humanoids is interesting because it intertwines so many different players: from the big tech giants to EV leaders, industrial conglomerates to specialized chip accelerators and everything in between. The landscape includes multi-centennial industrial incumbents, high burn VC darlings, and hardware-software integrators all angling for a slice of the humanoid pie from varied starting positions. These players all have different rights to win in different subcategories and trade at wildly different valuations.

While I'm primarily interested in finding private market investment opportunities, large swaths of the humanoid value chain will inevitably be dominated by large public incumbents. By analyzing the market structure, we can try to tease out where to park money in undervalued public names for above average compounding via tangential humanoid exposure vs. hunt for emerging pure-play disruptors in the private markets.

A few initial observations or themes before we dive into the specific categories:

- Geographic Strengths

- US companies lead in foundation models and high-end chip design. China leads in scaled manufacturing and low-cost components. Japan, Germany and Korea lead in high-end precision tooling. Today's market map tends to reflect these relative competitive advantages.

- However, one should keep in mind that investing contra these strengths may also be rational based on fragmenting global supply chains as regional hegemons aim to reduce existing dependencies and foster domestic champions in areas of relative weakness.

- Concentration vs. Fragmentation

- This early in an industry S-curve it’s difficult to forecast whether the ultimate market structure for humanoids ends up closer to smart phones (OS duopoly) or automobiles (greater fragmentation / competition and lower margins)

- Given the diversity of use cases - logistics, manufacturing, construction, hospitality, consumer, etc - greater market fragmentation seems likely based on relative specialization catering to different designs and feedback loops. At the same time, the greater variability in expected performance should lead to more meaningful pricing power for leaders in each category. I would expect something in between EVs and smartphones - several dominant vertically integrated companies and then dominant, open models which run many different hardware combinations.

- Vertical Integration vs. Modular Value Chains

- To me, similar to what we have seen in AI, closed, vertically-integrated approaches are likely to sprint ahead in many end markets given the feedback loops between hardware and software and designing each with the other in mind (i.e. sensors designed for particular hands which focus on collecting data for specific tasks and feedback into the model which can further inform more tailored chips or sensors, etc). These feedback loops are likely to be faster in closed, vertically integrated ecosystems leading to better early performance. Ostensibly this is why Brett Adcock terminated his agreement with OpenAI.

- Over-time, however, modular supply chains atop open standards will take share based on cost efficiencies. This is where China's industrial capacity, dense supplier networks, and scale come into play. Joe Ryu makes a compelling argument that vertically integrating too early is a mistake: leading to an oligopoly market structure with less dynamic experimentation. This a greater risk within the US as opposed to China.

- Paradoxically, this may prove great for early US investors in the vertically integrated leaders but ultimately lead to a more fragile ecosystem and lower long-term volumes compared to the Chinese strategy of "letting 1000 flowers bloom" in target industries, forcing companies through the gladiatorial area of provincial competition. Given the overlap in supply chains, the EV industry is instructive. Tesla alone is currently worth 3-4x more than the entire Chinese EV industry, but China is the cost and volume leader set to take increasing global share at price points with which western leaders cannot compete (absent tariffs). The data feedback loops of real-world robotics could make this a compelling strategy to pursue.

- We have witnessed a similar pattern playout in smart phones where Apple's tight integration created trillions in shareholder value, but now must rely on ecosystem lock-in to maintain share as on product quality, combinations of Android, Samsung, Huawei, and Xiaomi are clearly superior. My suspicion is that Chinese competition will be even faster and more formidable in robotics vs. EVs and smart phones given the strategic nature of the industry and Chinese leaderships existential race against an aging labor force and limited societal appetite for immigration and assimilation.

- Valuations aside: short-term, I'm more bullish on US vertically integrated OEMs and overseas component suppliers. Medium to long-term, China's ecosystem appears poised to lead on costs with a data feedback loop which will prove formative with leading volumes.

- Relative Valuation Gap

- The US valuations reflect this dynamic and appear significantly more inflated today relative to their Chinese counterparts. Figure AI recently raised was rumored to have raised >US$b at a ~US$39b. Companies in China with similar capabilities - like AgiBot - are valued at ~10b RMB (~US$1.5b). China's leader Unitree is rumored to be seeking a listing at the ~50b RMB range (~US$7b)

- Early Use Cases

- Given the price point, security concerns, highly varied layouts, and regulatory burden, consumer humanoids are likely much further away compared with industrial and business use cases where humanoids can be safely siloed and monitored within more predictable settings and priced with a more obvious ROI.

- General Purpose vs. Specialized Robots

- Near term, specialized robots may outperform, but longer-term, it seems highly likely that the versatility and economies of scale of general purpose humanoids will provide a much larger market. Mechanism Capital outlines the reasons why in more detail in this article. The pattern is clear:

.png)

.png)

Early Pockets to Watch:

We will be diving deeper into both the software and hardware component ecosystems in coming reports, but based on this profit pool sizing exercise and mapping of the market structure, below are a few categories which appear ripe for further inspection:

- Perception/Tactile sensors

- Actuation & transmissions (roller screws/reducers, especially the hands)

- Embodied AI Foundation Model Inputs and Robot Operating Systems

- Fleet Operation Software + Teleoperations

- Edge inference

1. Perception and sensing (vision, depth, e-skin)

Why: safety + dexterity requirements will mandate richer sensing; many “missing” modules (i.e. e-skin, robust low-cost depth) have no default supplier yet.

Structure: commodity cameras exist, but robot-grade multimodal sensing (durable, low-latency, integrated) is under-served.

Private investment angle: novel hardware sensors - particularly around tactile / force (companies like SynTouch or GelSight) as well as more integrated stacks with proprietary software like Slamcore or Navvis.

2. Actuation & transmissions

Why: Actuation + reducers = ~33% of BOM; each humanoid needs ~40+ joints/actuators. Capacity is supply-constrained and geographically concentrated.

Structure: concentrated legacy vendors; volume/cost roadmap not yet ready for ramp - new designs or Western capacity build-out.

Private investment angle: back novel transmissions, dexterous hands ****leaders, Western roller-screw capacity, integrated joint modules.

3. Foundational autonomy & Robot OS

Why: Perhaps the biggest remaining unlock for many embodied AI use cases is true multimodal intelligence. Many OEMs will vertically integrate with their own models, but open platforms will also compete. As fleets scale, recurring software revenues (motion/skills packs, updates, analytics) will compound, and the race remains open

Structure: pre-Android: fragmented, OEMs building in-house out of necessity.

Private investment angle: embodied-AI foundation models, skill libraries, planning/motion stacks, and a real OS/middleware with app distribution. Similar to AI, real-data suppliers also appear to be a meaningful bottleneck

4. Edge inference & on-robot compute platforms

Why: humanoids are edge-first for latency/cost; mid-power chips that run VLMs/skills locally at an acceptable performance per dollar will need to ramp considerably

Structure: Nvidia leading but room for domain specific edge NPUs at decent costs.

Private investment angle: chips/modules + compilers that squeeze real-time pipelines on device.

5. Fleet ops & teleoperations

Why: as deployments scale, fleet management - likely across heterogeneous robots and software - uptime, scheduling, tele-assist, billing - becomes more essential

Structure: service businesses reward execution over deep IP; customers likely keen to reduce single vendor lock-in and sticky once embedded

Private investment angle: verticalized "robot-as-a-service" vendors, cross-OEM fleet orchestration, 24/7 teleops, predictive maintenance platforms.

Riding the Wave

In a market this large, an investment door this narrow, and AI capabilities continuing to compound, humanoids are poised to command one of the largest investment cycles in history. Similar to the GPU and AI waves, capital allocation sentiment will likely go from “slight growth tailwinds” to “I’m under-allocated and my job is at risk” in fairly short-order.

At the same time, today’s hype outpaces the current capabilities as many investors do not fully comprehend the extreme technical difficulties still required to scale intelligent humanoids globally.

In this series, we outline our findings and thoughts in real-time about what is likely to be one of the most consequential industries in history and where we believe are the most attractive pockets to find exposure in an investment cycle much too large to dismiss.

Exposure is non-negotiable and yet treacherous. Hopefully our learnings can help both you and us to find footholds which lead to the summit 🙂

Part II on Humanoid Software Enablers coming next month.

.png)